Show code

try:

import yfinance, pandas, pandas_datareader

except Exception:

!pip -q install yfinance pandas pandas-datareaderBuild a Reliable Pipeline with Free APIs (Colab Version)

This is the Colab version using free APIs (yfinance). For the in-class Bloomberg Terminal session (Excel add-in), see Lab 2: Survivorship Bias in UK Banking.

Expected Time:

![]()

Ulster students have access to ~20 Bloomberg terminals in the Financial Innovation Lab. The in-class Week 2 lab uses the Bloomberg Excel add-in to quantify survivorship bias with UK banking crisis data: Lab 2: Survivorship Bias in UK Banking.

try:

import yfinance, pandas, pandas_datareader

except Exception:

!pip -q install yfinance pandas pandas-datareaderReal-world financial data science starts with data acquisition. APIs are your gateway to market data, but they’re unreliable: rate limits, outages, data quality issues. Professional systems need resilience: retry logic, fallback sources, validation, and logging.

1. Resilience → Handle API failures gracefully (retries, fallbacks, synthetic data)

2. Validation → Check data quality before analysis (missing values, outliers, gaps)

3. Provenance → Log data sources and transformations (reproducibility, debugging)

These aren’t optional extras: they’re the difference between research toys and production systems.

By the end of this lab, you will have:

Time estimate: ≈ 60 minutes (plus optional extensions)

In projects and assessments, you’ll often build models (or trading rules) on top of a data pipeline. If your pipeline has silent bugs (wrong dates, missing values, look-ahead bias), your entire analysis is invalidated. Build good habits now.

This task implements a resilient data pipeline: try yfinance first, fall back to Stooq if it fails, use synthetic data as last resort. This three-tier approach ensures your analysis never stops due to API failures.

Why we need fallbacks: - Free APIs have rate limits (yfinance: ~2000 calls/hour) - APIs go down (maintenance, outages, deprecated endpoints) - Network issues are common in cloud environments

Three-tier strategy: 1. Primary: yfinance (best for US equities, free, widely used) 2. Fallback: Stooq via pandas-datareader (alternative free source) 3. Last resort: Synthetic data (ensures code always runs for testing)

This pattern appears in production systems at every scale.

import os, time, random

import yfinance as yf

import pandas as pd

import numpy as np

symbols = ['AAPL', 'MSFT', 'SPY']

def get_close_from_yf(symbols, period='2y', tries=3):

"""

Fetch adjusted closing prices from Yahoo Finance with retry logic.

Implements exponential backoff to handle rate limits gracefully. Returns

adjusted prices (splits/dividends applied) suitable for return calculations.

Parameters

----------

symbols : list of str

Stock tickers (e.g., ['AAPL', 'MSFT'])

period : str, default='2y'

Data period: '1d', '5d', '1mo', '3mo', '6mo', '1y', '2y', '5y', '10y', 'ytd', 'max'

tries : int, default=3

Number of retry attempts before raising error

Returns

-------

pd.DataFrame

Adjusted closing prices with DatetimeIndex and symbol columns

Raises

------

RuntimeError

If all retry attempts fail

Notes

-----

- Uses `auto_adjust=True` to get split/dividend-adjusted prices

- Implements exponential backoff: waits 2, 4, 6 seconds between retries

- Handles yfinance MultiIndex columns (multiple symbols) vs single-symbol format

- Returns empty rows are filtered (only keeps days with at least one price)

Examples

--------

>>> prices = get_close_from_yf(['AAPL', 'MSFT'], period='1y')

>>> prices.shape

(252, 2) # Roughly 252 trading days in a year

>>> prices.iloc[-1] # Most recent closing prices

AAPL 182.50

MSFT 415.20

"""

last_err = None

for attempt in range(tries):

try:

# Download with adjusted prices (splits/dividends applied)

df = yf.download(symbols, period=period, auto_adjust=True,

progress=False, group_by='ticker', threads=True)

# yfinance returns MultiIndex columns when fetching multiple symbols

if isinstance(df.columns, pd.MultiIndex):

# Extract 'Close' price for each symbol

closes = pd.concat(

{sym: df[sym]['Close'] for sym in symbols if sym in df.columns.levels[0]},

axis=1

)

closes.columns = [c if isinstance(c, str) else c[0] for c in closes.columns]

else:

# Single symbol returns simple columns

closes = df['Close'].to_frame(symbols[0])

# Only return if we got at least one non-empty row

if closes.dropna(how='all').shape[0] > 0:

return closes

except Exception as e:

last_err = e

# Exponential backoff with jitter to avoid thundering herd

time.sleep(2 * (attempt + 1) + random.random())

raise RuntimeError(f"yfinance download failed after {tries} tries: {last_err}")

def get_close_from_stooq(symbols, years=2):

"""

Fetch closing prices from Stooq via pandas-datareader (fallback source).

Stooq provides historical price data for global markets. This function

serves as fallback when yfinance fails. Fetches data sequentially to

respect rate limits.

Parameters

----------

symbols : list of str

Stock tickers (e.g., ['AAPL', 'MSFT'])

years : int, default=2

Number of years of historical data to fetch

Returns

-------

pd.DataFrame

Closing prices with DatetimeIndex (sorted) and symbol columns

Raises

------

RuntimeError

If no symbols successfully fetched

Notes

-----

- Fetches symbols sequentially (not parallel) to respect rate limits

- Waits 0.4 seconds between requests

- Silently skips symbols that fail (rather than stopping entire process)

- Returns only successfully fetched symbols

Examples

--------

>>> prices = get_close_from_stooq(['AAPL'], years=1)

>>> prices.index.name

'Date'

"""

from datetime import datetime, timedelta

from pandas_datareader import data as web

# Define date range

end = datetime.today()

start = end - timedelta(days=365 * years + 14) # Extra days for weekends/holidays

series = []

for sym in symbols:

try:

# Fetch from Stooq and extract 'Close' column

s = web.DataReader(sym, 'stooq', start, end)['Close'].sort_index()

s.name = sym

series.append(s)

# Respectful rate limiting

time.sleep(0.4)

except Exception:

# Skip symbols that fail rather than stopping entire fetch

pass

if not series:

raise RuntimeError("stooq fallback returned no data")

return pd.concat(series, axis=1)

def synthetic_prices(symbols, periods=252, mu=0.0004, sigma=0.012):

"""

Generate synthetic price series using geometric Brownian motion.

This is a last-resort fallback when all real APIs fail. Useful for

testing and development when APIs are unavailable. NOT FOR ANALYSIS.

Parameters

----------

symbols : list of str

Symbol names for columns (can be anything)

periods : int, default=252

Number of business days to generate (~1 year of trading days)

mu : float, default=0.0004

Daily drift (mean return): 0.0004 ≈ 10% annual

sigma : float, default=0.012

Daily volatility: 0.012 ≈ 19% annual volatility

Returns

-------

pd.DataFrame

Synthetic prices starting at 100, with business day index

Notes

-----

- Uses fixed seed (42) for reproducibility

- Generates prices via: P(t) = 100 * exp(cumsum(returns))

- Returns ~ Normal(mu, sigma) independently across symbols

- Index: business days ending at today

Examples

--------

>>> synth = synthetic_prices(['SYN1', 'SYN2'], periods=10)

>>> synth.shape

(10, 2)

>>> (synth.iloc[-1] / synth.iloc[0]).mean() # Typical growth

1.04 # Roughly 4% over 10 days

Warnings

--------

DO NOT use for actual analysis. This is for code testing only.

"""

rng = np.random.default_rng(42) # Fixed seed for reproducibility

# Business day index ending today

dates = pd.bdate_range(end=pd.Timestamp.today().normalize(), periods=periods)

# Generate returns: Normal(mu, sigma)

shocks = rng.normal(mu, sigma, size=(len(dates), len(symbols)))

# Convert to prices: P(t) = P(0) * exp(cumsum(returns))

levels = 100 * np.exp(np.cumsum(shocks, axis=0))

return pd.DataFrame(levels, index=dates, columns=symbols)# === Try primary source (yfinance) ===

try:

prices = get_close_from_yf(symbols)

source = 'yfinance'

print(f"✔ Successfully fetched from yfinance")

except Exception as e1:

print(f"⚠ yfinance failed: {e1}")

# === Try fallback source (Stooq) ===

try:

prices = get_close_from_stooq(symbols)

source = 'stooq (pandas-datareader)'

print(f"✔ Successfully fetched from Stooq fallback")

except Exception as e2:

print(f"⚠ Stooq failed: {e2}")

# === Last resort: synthetic data ===

prices = synthetic_prices(symbols)

source = f'synthetic (fallback due to API failures)'

print(f"⚠ Using synthetic data (NOT for real analysis!)")

# Display first and last few rows

print(f"\nData shape: {prices.shape}")

print(f"\nFirst 3 rows:")

print(prices.head(3))

print(f"\nLast 3 rows:")

print(prices.tail(3))⚠ yfinance failed: yfinance download failed after 3 tries: None

✔ Successfully fetched from Stooq fallback

Data shape: (511, 3)

First 3 rows:

AAPL MSFT SPY

Date

2024-02-28 179.953 405.442 498.350

2024-02-29 179.286 411.329 500.142

2024-03-01 178.207 413.179 504.838

Last 3 rows:

AAPL MSFT SPY

Date

2026-03-10 260.72 405.76 677.18

2026-03-11 260.81 404.88 676.33

2026-03-12 255.76 401.86 666.06The try-except cascade ensures you always get data, even if APIs fail. In production, you’d add alerts when fallbacks activate so engineers can investigate the primary failure.

# === Build provenance log ===

log = {}

log['source'] = source

log['symbols_requested'] = len(symbols)

log['symbols_received'] = len(prices.columns)

log['date_range'] = f"{prices.index[0]} to {prices.index[-1]}"

log['trading_days'] = len(prices)

# === Check for missing prices ===

log['missing_prices'] = int(prices.isna().sum().sum())

log['missing_pct'] = f"{(prices.isna().sum().sum() / prices.size * 100):.2f}%"

# === Calculate returns and check quality ===

rets = prices.pct_change()

log['missing_returns'] = int(rets.isna().sum().sum())

# === Flag outliers (|return| > 20% = likely data error or halt) ===

log['out_of_range'] = int((rets.abs() > 0.2).sum().sum())

# Display log

import json

print("\n=== Data Quality Log ===")

print(json.dumps(log, indent=2))

# === Quality gate ===

if prices.dropna(how='all').shape[0] > 0:

print(f"\n✔ Data source: {source}")

print(f"✔ Download and validation checks passed")

else:

print(f"\n⚠ Warning: no data returned from any source")

=== Data Quality Log ===

{

"source": "stooq (pandas-datareader)",

"symbols_requested": 3,

"symbols_received": 3,

"date_range": "2024-02-28 00:00:00 to 2026-03-12 00:00:00",

"trading_days": 511,

"missing_prices": 0,

"missing_pct": "0.00%",

"missing_returns": 3,

"out_of_range": 0

}

✔ Data source: stooq (pandas-datareader)

✔ Download and validation checks passedRule of thumb: <1% missing is acceptable, >5% requires investigation

Checkpoint: Look at your log. Which quality issues did you find? How would you handle them differently for a production system vs. academic analysis?

Raw data always has issues. Professional practice: clean conservatively and document decisions.

# === Remove rows where all returns are missing ===

clean = rets.dropna()

print(f"Original shape: {rets.shape}")

print(f"After dropna: {clean.shape}")

print(f"Rows removed: {rets.shape[0] - clean.shape[0]}")

# === Clip extreme values (conservative approach) ===

# Instead of deleting outliers, cap them at reasonable limits

# -20% to +20% captures 99%+ of normal daily returns

clean_clipped = clean.clip(lower=-0.2, upper=0.2)

# Count how many values were clipped

clipped_low = (clean < -0.2).sum().sum()

clipped_high = (clean > 0.2).sum().sum()

print(f"\n=== Outlier Treatment ===")

print(f"Values clipped at lower bound (-20%): {clipped_low}")

print(f"Values clipped at upper bound (+20%): {clipped_high}")

# Display sample

print(f"\nCleaned returns (last 5 days):")

print(clean_clipped.tail())Original shape: (511, 3)

After dropna: (510, 3)

Rows removed: 1

=== Outlier Treatment ===

Values clipped at lower bound (-20%): 0

Values clipped at upper bound (+20%): 0

Cleaned returns (last 5 days):

AAPL MSFT SPY

Date

2026-03-06 -0.010720 -0.004992 -0.013107

2026-03-09 0.009438 0.001762 0.008760

2026-03-10 0.003194 -0.008770 -0.001607

2026-03-11 0.000345 -0.002169 -0.001255

2026-03-12 -0.019363 -0.007459 -0.015185# === Save to CSV for later use ===

clean_clipped.to_csv('returns_clean.csv')

# === Verify file was created ===

import os

if os.path.exists('returns_clean.csv'):

file_size = os.path.getsize('returns_clean.csv')

print(f"✔ Saved returns_clean.csv ({file_size:,} bytes)")

else:

print("⚠ Warning: File not created")

# === Document the cleaning process ===

cleaning_log = {

'rows_original': rets.shape[0],

'rows_after_dropna': clean.shape[0],

'values_clipped_low': int(clipped_low),

'values_clipped_high': int(clipped_high),

'clip_bounds': '[-20%, +20%]',

'output_file': 'returns_clean.csv'

}

print(f"\n=== Cleaning Summary ===")

print(json.dumps(cleaning_log, indent=2))✔ Saved returns_clean.csv (38,609 bytes)

=== Cleaning Summary ===

{

"rows_original": 511,

"rows_after_dropna": 510,

"values_clipped_low": 0,

"values_clipped_high": 0,

"clip_bounds": "[-20%, +20%]",

"output_file": "returns_clean.csv"

}Deliverable: Write a short note (100-150 words) describing: - What issues you found (missing values, outliers) - How you handled them (dropna, clipping) - Why these choices are appropriate for financial return data - What trade-offs you made (e.g., information loss vs. robustness)

auto_adjust=True.This short exercise previews a factor dataset (JKP). Load a small sample CSV, compute quick stats, and (optionally) run a one‑line CAPM alpha.

# JKP sample (course mirror) : small monthly slice with MKT, SMB, HML, MOM

import pandas as pd, os

import statsmodels.api as sm

# Prefer local file during site build; fall back to raw GitHub if needed

local_path = os.path.join('..','resources','jkp-sample.csv')

if os.path.exists(local_path):

jkp = pd.read_csv(local_path, parse_dates=['date']).set_index('date').sort_index()

else:

# Use public notebooks repo URL for Colab

url = "https://raw.githubusercontent.com/quinfer/fin510-colab-notebooks/main/resources/jkp-sample.csv"

jkp = pd.read_csv(url, parse_dates=['date']).set_index('date').sort_index()

# Summary stats and quick cumulative return for MOM

summary = jkp[['MKT','SMB','HML','MOM']].describe().round(3)

cum = (1 + jkp['MOM']).cumprod() - 1

summary.tail(3), cum.tail()

# Optional: CAPM alpha (no HAC here : use HAC in the assessment)

ls = jkp['MOM'].dropna()

mkt = jkp['MKT'].reindex(ls.index)

capm = sm.OLS(ls, sm.add_constant(mkt)).fit()

float(capm.params['const']), float(capm.tvalues['const'])(0.005408343449950338, 1.763810502676042)Notes - In the assessment you will use a larger CSV downloaded from the JKP portal and apply HAC standard errors. - Keep scope tight (few factors, limited window) and focus on quality of evidence.

# Ensure prediction tasks shift the target correctly

import pandas as pd

# Intentionally wrong design (no shift) for demonstration

X_wrong = jkp[['MKT','SMB','HML','MOM']].dropna()

y_next = jkp['MOM'].shift(-1) # next-month target

# Overlap of indices indicates potential leakage if you don't drop/shift properly

overlap = X_wrong.index.intersection(y_next.dropna().index)

print("Potential leakage rows with wrong design:", len(overlap))

# Correct design: predictors at t, target at t+1 → align and drop NA

X = jkp[['MKT','SMB','HML']].shift(0)

y = jkp['MOM'].shift(-1)

df = pd.concat([X, y.rename('y')], axis=1).dropna()

print("Rows after proper shift/drop:", len(df))Potential leakage rows with wrong design: 9

Rows after proper shift/drop: 9This extension connects to the lecture material on empirical regularities in financial returns. Before analysing any financial dataset, you should verify it exhibits the known stylised facts.

Financial returns consistently show:

These are empirical facts, not assumptions. Your data should exhibit them.

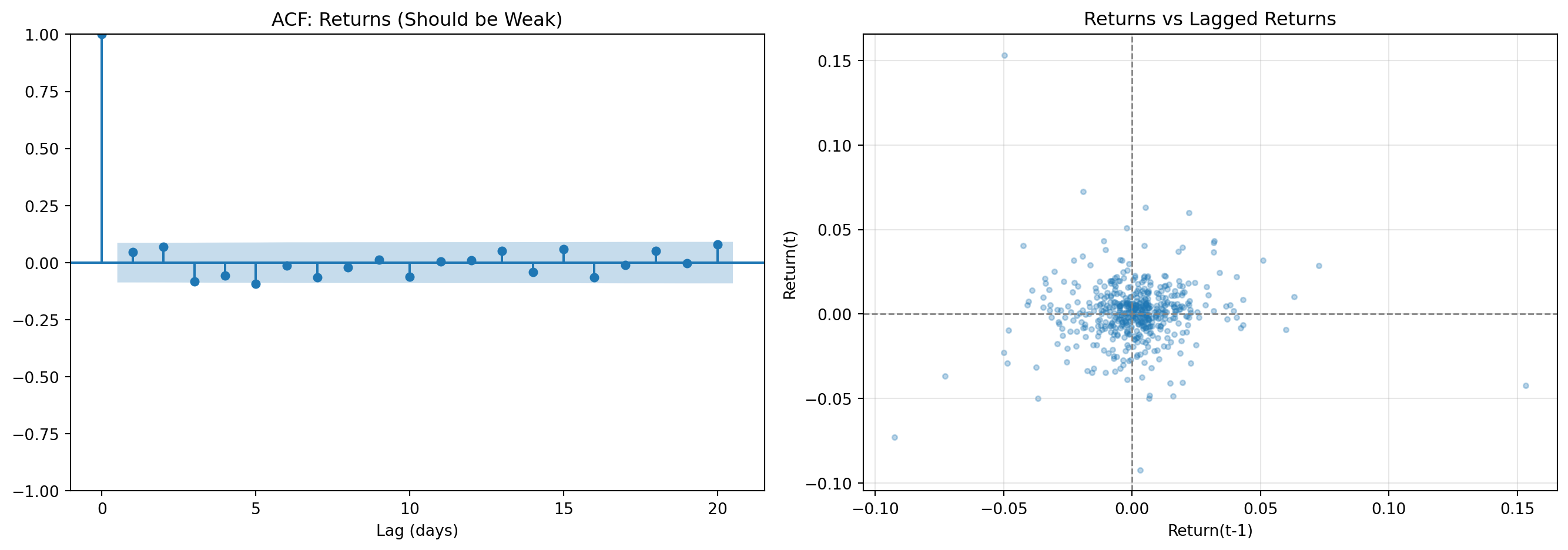

from statsmodels.graphics.tsaplots import plot_acf

import matplotlib.pyplot as plt

# Use one asset from your cleaned returns

returns_series = clean_clipped.iloc[:, 0].dropna() # First column

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

# ACF of returns (should be weak)

ax1 = axes[0]

plot_acf(returns_series, lags=20, ax=ax1, alpha=0.05)

ax1.set_title('ACF: Returns (Should be Weak)')

ax1.set_xlabel('Lag (days)')

# Scatter plot: r(t) vs r(t-1)

ax2 = axes[1]

ax2.scatter(returns_series.shift(1), returns_series, alpha=0.3, s=10)

ax2.axhline(y=0, color='gray', linestyle='--', lw=1)

ax2.axvline(x=0, color='gray', linestyle='--', lw=1)

ax2.set_xlabel('Return(t-1)')

ax2.set_ylabel('Return(t)')

ax2.set_title('Returns vs Lagged Returns')

ax2.grid(alpha=0.3)

plt.tight_layout()

plt.show()

# Quantify

lag1_corr = returns_series.autocorr(lag=1)

print(f"\nLag-1 autocorrelation: {lag1_corr:.4f}")

print("Interpretation: Near zero → returns are approximately unpredictable")

Lag-1 autocorrelation: 0.0459

Interpretation: Near zero → returns are approximately unpredictable# Compare ACF of returns vs squared returns (volatility proxy)

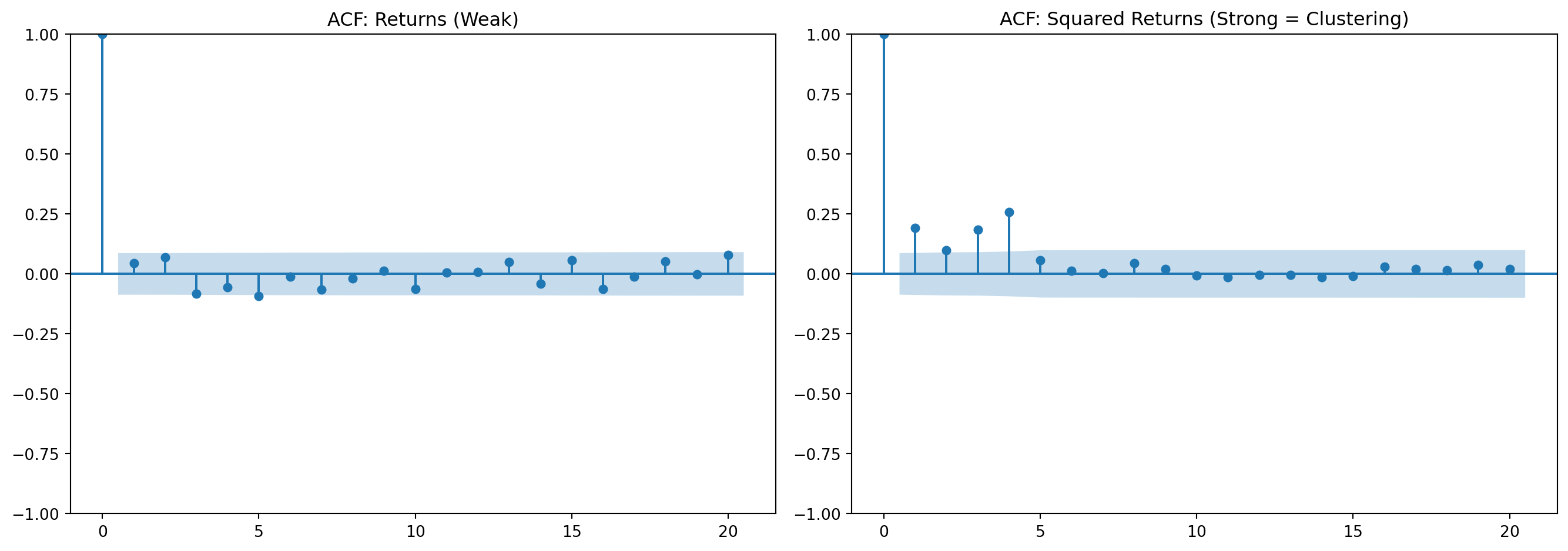

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

ax1 = axes[0]

plot_acf(returns_series, lags=20, ax=ax1, alpha=0.05)

ax1.set_title('ACF: Returns (Weak)')

ax2 = axes[1]

plot_acf(returns_series**2, lags=20, ax=ax2, alpha=0.05)

ax2.set_title('ACF: Squared Returns (Strong = Clustering)')

plt.tight_layout()

plt.show()

# Quantify

acf_ret_lag1 = returns_series.autocorr(lag=1)

acf_sq_lag1 = (returns_series**2).autocorr(lag=1)

print(f"\nReturns ACF(1): {acf_ret_lag1:.4f}")

print(f"Squared returns ACF(1): {acf_sq_lag1:.4f}")

print("\nInterpretation: Squared returns show strong persistence → volatility clustering")

print("This is why GARCH models are needed for volatility forecasting")

Returns ACF(1): 0.0459

Squared returns ACF(1): 0.1908

Interpretation: Squared returns show strong persistence → volatility clustering

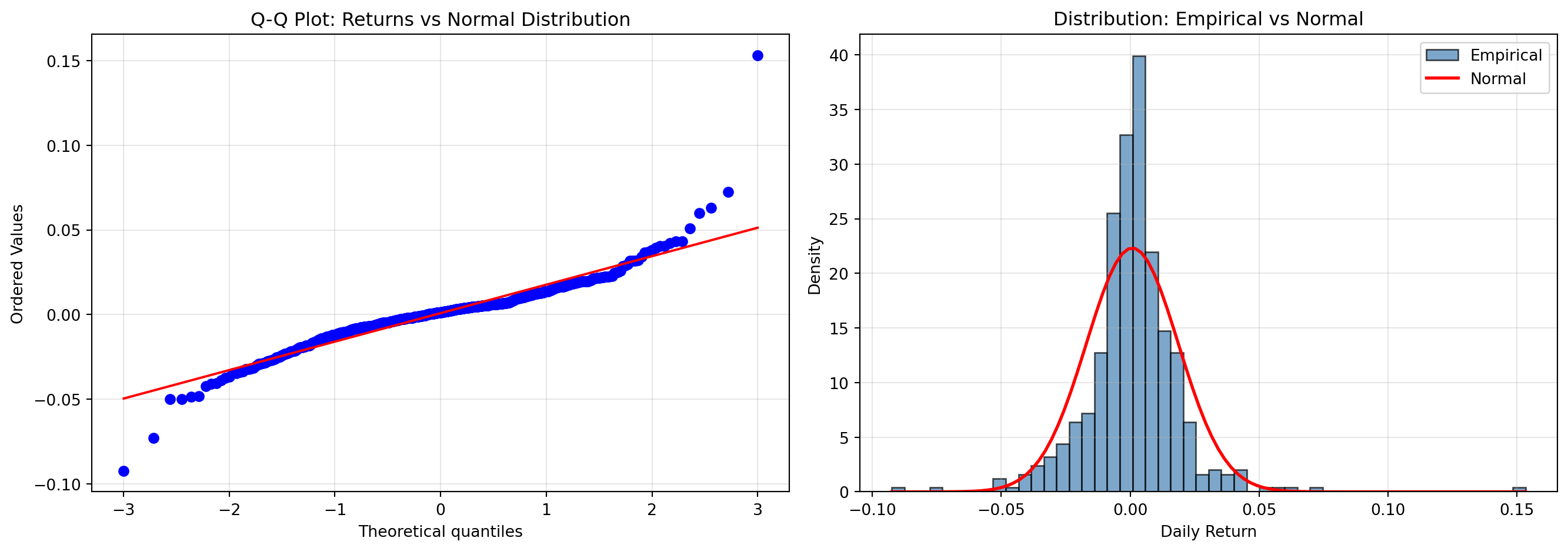

This is why GARCH models are needed for volatility forecastingfrom scipy import stats

fig, axes = plt.subplots(1, 2, figsize=(14, 5))

# Q-Q plot (curved ends = fat tails)

ax1 = axes[0]

stats.probplot(returns_series, dist="norm", plot=ax1)

ax1.set_title('Q-Q Plot: Returns vs Normal Distribution')

ax1.grid(alpha=0.3)

# Histogram vs Normal

ax2 = axes[1]

ax2.hist(returns_series, bins=50, density=True, alpha=0.7,

color='steelblue', label='Empirical', edgecolor='black')

x = np.linspace(returns_series.min(), returns_series.max(), 100)

ax2.plot(x, stats.norm.pdf(x, returns_series.mean(), returns_series.std()),

'r-', lw=2, label='Normal')

ax2.set_xlabel('Daily Return')

ax2.set_ylabel('Density')

ax2.set_title('Distribution: Empirical vs Normal')

ax2.legend()

ax2.grid(alpha=0.3)

plt.tight_layout()

plt.show()

# Quantify

kurtosis = returns_series.kurtosis()

_, p_norm = stats.normaltest(returns_series)

print(f"\nExcess kurtosis: {kurtosis:.2f} (Normal = 0)")

print(f"Normality test p-value: {p_norm:.4f}")

if p_norm < 0.05:

print("→ Reject normality: fat tails are present")

else:

print("→ Cannot reject normality (unusual for financial data)")

Excess kurtosis: 12.76 (Normal = 0)

Normality test p-value: 0.0000

→ Reject normality: fat tails are present# Skewness analysis

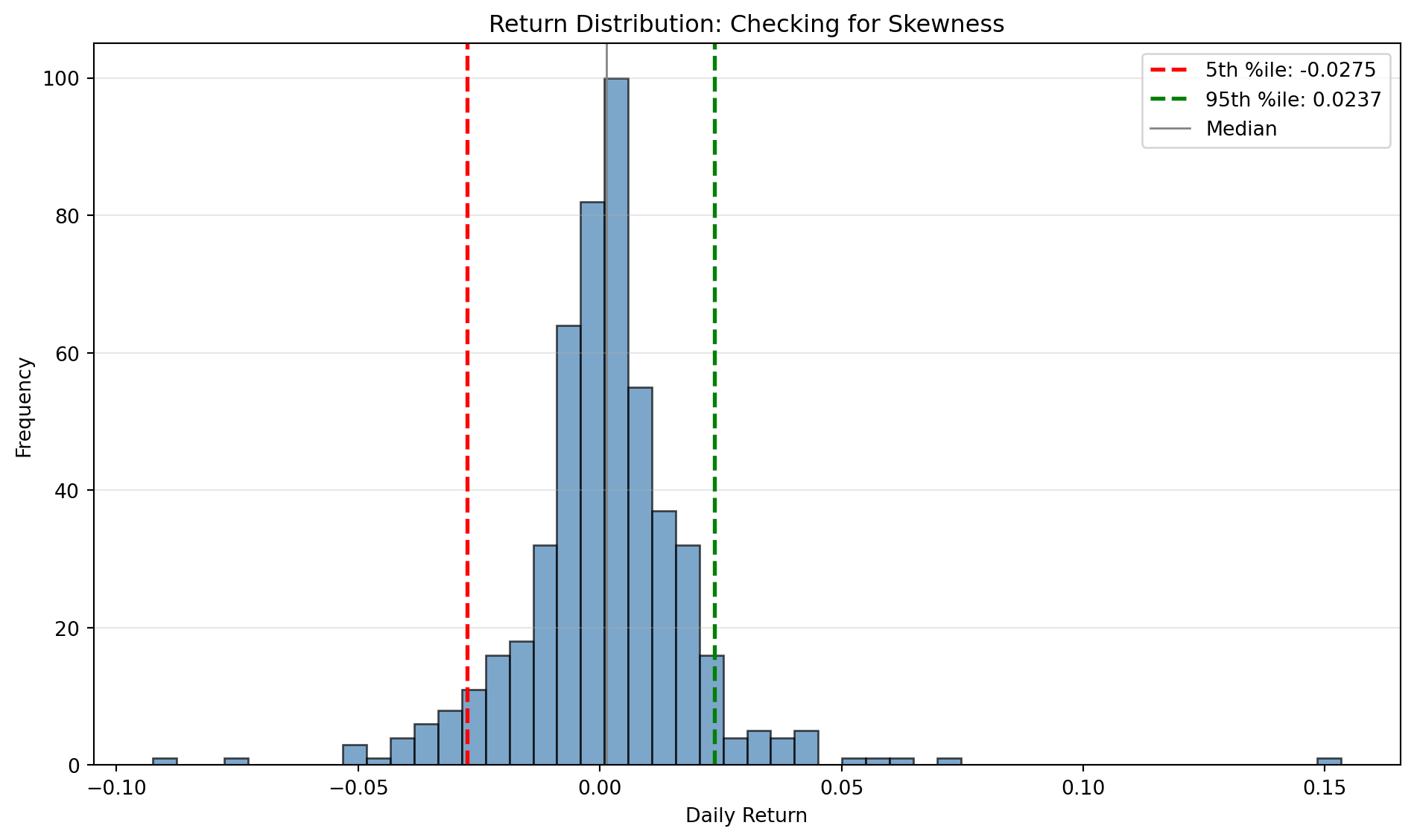

skewness = returns_series.skew()

# Compare tail quantiles

left_5pct = float(returns_series.quantile(0.05))

right_5pct = float(returns_series.quantile(0.95))

median_val = float(returns_series.median())

fig, ax = plt.subplots(figsize=(10, 6))

ax.hist(returns_series, bins=50, alpha=0.7, color='steelblue', edgecolor='black')

ax.axvline(x=left_5pct, color='red', linestyle='--', lw=2,

label=f'5th %ile: {left_5pct:.4f}')

ax.axvline(x=right_5pct, color='green', linestyle='--', lw=2,

label=f'95th %ile: {right_5pct:.4f}')

ax.axvline(x=median_val, color='gray', linestyle='-', lw=1, label='Median')

ax.set_xlabel('Daily Return')

ax.set_ylabel('Frequency')

ax.set_title('Return Distribution: Checking for Skewness')

ax.legend()

ax.grid(alpha=0.3, axis='y')

plt.tight_layout()

plt.show()

print(f"\nSkewness: {skewness:.3f}")

if skewness < 0:

print("→ Negative skewness: left tail is longer (crashes > melt-ups)")

else:

print("→ Positive skewness: right tail is longer (unusual)")

print(f"\nLeft tail (5th %ile): {left_5pct:.4f}")

print(f"Right tail (95th %ile): {right_5pct:.4f}")

print(f"Tail asymmetry: {abs(left_5pct) / abs(right_5pct):.2f}")

Skewness: 0.898

→ Positive skewness: right tail is longer (unusual)

Left tail (5th %ile): -0.0275

Right tail (95th %ile): 0.0237

Tail asymmetry: 1.16# Summary of all stylised facts

print("=" * 60)

print("STYLISED FACTS VERIFICATION SUMMARY")

print("=" * 60)

print(f"\n1. Return Autocorrelation (Lag 1): {acf_ret_lag1:.4f}")

if abs(acf_ret_lag1) < 0.1:

print(" ✓ PASS: Weak autocorrelation (returns unpredictable)")

else:

print(" ⚠ CHECK: Strong autocorrelation detected")

print(f"\n2. Volatility Clustering ACF (Lag 1): {acf_sq_lag1:.4f}")

if acf_sq_lag1 > 0.1:

print(" ✓ PASS: Volatility clustering present")

else:

print(" ⚠ CHECK: Weak volatility clustering")

print(f"\n3. Excess Kurtosis: {kurtosis:.2f}")

if kurtosis > 1:

print(" ✓ PASS: Fat tails present (kurtosis > 1)")

else:

print(" ⚠ CHECK: Tails may not be fat enough")

print(f"\n4. Skewness: {skewness:.3f}")

if skewness < 0:

print(" ✓ PASS: Negative skewness (crash risk > upside)")

else:

print(" ⚠ CHECK: Positive or zero skewness (unusual)")

print(f"\n5. Normality Test p-value: {p_norm:.4f}")

if p_norm < 0.05:

print(" ✓ PASS: Non-normal distribution (expected)")

else:

print(" ⚠ CHECK: Cannot reject normality (unusual for returns)")

print("\n" + "=" * 60)

print("\nIf your data passes most checks, it exhibits realistic properties.")

print("If not, investigate: data errors? wrong frequency? synthetic data?")============================================================

STYLISED FACTS VERIFICATION SUMMARY

============================================================

1. Return Autocorrelation (Lag 1): 0.0459

✓ PASS: Weak autocorrelation (returns unpredictable)

2. Volatility Clustering ACF (Lag 1): 0.1908

✓ PASS: Volatility clustering present

3. Excess Kurtosis: 12.76

✓ PASS: Fat tails present (kurtosis > 1)

4. Skewness: 0.898

⚠ CHECK: Positive or zero skewness (unusual)

5. Normality Test p-value: 0.0000

✓ PASS: Non-normal distribution (expected)

============================================================

If your data passes most checks, it exhibits realistic properties.

If not, investigate: data errors? wrong frequency? synthetic data?Write a brief note (150-200 words) answering:

Submit via Blackboard if completing for credit.

This extension directly applies concepts from:

You’ve now built a complete data pipeline with:

These patterns transfer to all financial data work : use them in every future analysis.

Next lab: Quantify survivorship bias using Bloomberg Terminal (in-class, Excel add-in) or explore alternative data sources (homework extension).