---

title: "Foundations of Financial Data Science"

subtitle: "From Classical Econometrics to Modern Machine Learning"

author: "Professor Barry Quinn CStat"

date: today

format:

html:

toc: true

toc-depth: 3

toc-location: left

code-fold: true

code-summary: "Show Python code"

code-tools:

source: true

toggle: true

caption: none

execute:

warning: false

message: false

echo: true

eval: true

fig-width: 10

fig-height: 6

fig-format: png

jupyter: fin510

bibliography: ../resources/reading.bib

---

::: {.callout-tip}

## Chapter Overview

This chapter provides the statistical and econometric foundations for responsible data science in finance. It serves as both a review of core concepts from introductory econometrics and an extension into modern data science methods. The material here will be referenced throughout subsequent chapters as we build toward more advanced techniques.

**Two intellectual threads run through this chapter:**

1. **Cross-sectional econometrics** → Tree-based machine learning (Chapters 7-8)

2. **Time series econometrics** → Sequence learning and foundation models (Chapters 11-12)

Understanding these connections helps you see machine learning not as a separate discipline, but as a natural extension of the econometric toolkit you already possess.

:::

::: {.callout-note}

#### View Slides

Open the lecture deck: [Week 1: Foundations of Financial Data Science](../slides/week01_foundations.qmd)

:::

```{python}

#| label: setup-data-root

#| include: false

import sys

from pathlib import Path

import yaml

try:

with open(Path("config/data_root.yml")) as f:

cfg = yaml.safe_load(f)

data_root = Path(cfg.get("data_root", "data")).expanduser().resolve()

except Exception:

data_root = Path("data")

sys.path.insert(0, str(Path("scripts").resolve()))

from bloomberg_loader import load_bloomberg

```

## Learning Objectives

By the end of this chapter, you should be able to:

- **Review and consolidate** core statistical concepts: distributions, estimation, hypothesis testing

- **Apply** regression analysis with appropriate diagnostics and interpretation

- **Recognise** when classical assumptions fail and understand the consequences

- **Explain** the bias-variance tradeoff and its implications for model selection

- **Contrast** frequentist and Bayesian perspectives on inference

- **Implement** regularisation and validation techniques for responsible modelling

- **Connect** classical econometric concepts to their machine learning extensions

# Part 0: Review of Statistical Foundations {#sec-foundations-review}

We take **data science** to mean the **disciplined study of variation and uncertainty in data**. Variation is what we model: differences across units, over time, between groups. Uncertainty is what we quantify: the limits of what we can know from finite samples and noisy measurements. This chapter consolidates the core statistical concepts that underpin that study in finance. This section serves as a reference point : material you may have encountered in introductory econometrics courses, now framed for the data science context. If you have completed an introductory course in econometrics, much of what follows will be familiar, though you may find the framing useful as we connect these foundations to the machine learning extensions that appear in later chapters.

## What Are We Really Trying to Do?

Every statistical analysis in finance confronts a version of the same fundamental problem: we have incomplete information about a complex system, and we need to make inferences that extend beyond what we directly observe. @gelman2020regression frame this challenge around three types of generalisation that appear, explicitly or implicitly, in nearly every quantitative analysis. First, we generalise from sample to population : the classic problem of statistical inference that pervades every study attempting to draw broad conclusions from limited data. Second, we generalise from treatment to control group, which is the essence of causal inference and lurks in the background of most regression interpretations even when we do not explicitly acknowledge it. Third, we generalise from observed measurements to underlying constructs, recognising that our data rarely capture exactly what we want to study. In finance, we might measure "volatility" using standard deviation, but does this truly capture the risk investors care about?

All three challenges can be reframed as prediction problems: predicting outcomes for observations not in our sample, predicting what would happen under alternative scenarios or interventions, and predicting underlying truth from noisy measurements. In finance, these challenges manifest constantly. When we observe returns for 100 stocks and attempt to say something about "the market," we face the first challenge. When a firm adopts a new strategy and performance subsequently improves, we wonder whether the strategy caused the improvement or whether other factors were responsible : the second challenge. When we quantify risk using historical volatility, we grapple with the third challenge: does our measurement truly reflect the construct we care about? Keeping these challenges in mind helps clarify what our analyses can and cannot tell us, and provides a useful frame for thinking about the extensions we develop in later chapters.

## Probability Distributions and the Machinery of Inference

Statistical inference begins with probability distributions : mathematical descriptions of how random variables behave. These distributions provide the language we use to quantify uncertainty, model returns, estimate parameters, and make inferences that extend beyond our sample. The Normal (Gaussian) distribution, parametrised by mean $\mu$ and variance $\sigma^2$, forms the foundation of classical inference through its symmetric, bell-shaped description of variation: $X \sim \mathcal{N}(\mu, \sigma^2)$. Financial returns are famously *not* normally distributed : they exhibit heavy tails and skewness that the Gaussian cannot capture : yet the Normal distribution remains central because of the Central Limit Theorem. As sample sizes grow, sample means become approximately normal regardless of the underlying distribution, which is why we can rely on normal-based inference even when individual observations are decidedly non-normal.

The Student's t-distribution extends this framework to account for a practical reality: when we estimate population variance from sample data, we introduce additional uncertainty. The t-distribution, with its heavier tails compared to the normal, reflects this extra layer of uncertainty through the relationship $t = \frac{\bar{X} - \mu}{s/\sqrt{n}} \sim t_{n-1}$. In finance, where we often analyse individual securities or short time periods with limited samples, this distinction matters for hypothesis testing : using the normal distribution when the t-distribution is appropriate understates our uncertainty and inflates our confidence in rejecting null hypotheses. The chi-squared distribution ($\chi^2$) arises naturally in variance estimation and goodness-of-fit tests, capturing the distribution of sums of squared standard normal variables: $(n-1)\frac{s^2}{\sigma^2} \sim \chi^2_{n-1}$. The F-distribution, defined as the ratio of two chi-squared variables scaled by their degrees of freedom, emerges when comparing variances or testing multiple restrictions simultaneously, and underpins joint hypothesis testing in regression analysis.

These distributions are not merely theoretical constructs : they are the tools we use to answer practical questions. Is an asset's expected return significantly different from zero? The t-test provides an answer. Do these factors jointly explain returns? The F-test addresses this question. Is the variance of returns stable over time? The chi-squared test offers evidence. Understanding *when* each distribution applies is as important as knowing the formulas themselves. The progression from sample statistic to test statistic to p-value is the essential machinery of frequentist inference, though as we shall see, this machinery comes with important limitations that deserve careful attention.

## Why Statistical Significance Misleads Practitioners

The concept of statistical significance pervades quantitative finance, yet @gelman2020regression argue that even experienced practitioners routinely fall into traps that undermine their inferences. The most common confusion conflates statistical significance with practical importance. A result can be "statistically significant" yet trivially small in economic terms : if an investment strategy earns 0.001% excess return with standard error 0.0003%, we can reject the null hypothesis at conventional levels (t ≈ 3.3), but the finding is economically meaningless once we account for transaction costs. The statistical machinery correctly identifies a non-zero effect, but tells us nothing about whether it matters in practice.

The converse error : interpreting non-significance as evidence of no effect : is equally problematic. Failure to reject the null hypothesis does not mean the effect is zero; it means the data are *inconclusive*. An estimate of 5% ± 8% (a confidence interval spanning from -3% to +13%) is consistent with both a large positive effect and a small negative one. Declaring that "there is no effect" based on p > 0.05 goes well beyond what the data support. A related but more subtle error pervades comparative analyses in finance research: the difference between "significant" and "not significant" is not itself statistically significant. If Strategy A has a significant alpha (t = 2.1) and Strategy B does not (t = 1.8), concluding that they differ meaningfully is incorrect without testing the *difference* directly. The standard error of a difference is typically larger (often by a factor of roughly √2) than the standard errors of the individual estimates, so two estimates that appear different based on their individual significance tests may not differ significantly when compared properly.

The flexibility inherent in data analysis creates further difficulties. Gelman and Loken describe the "garden of forking paths" : with enough flexibility in data processing, variable selection, and model specification, researchers can achieve p < 0.05 from almost any dataset, even pure noise. The problem is not always conscious "p-hacking" or deliberate fishing for significant results; rather, it arises from the accumulation of small, individually defensible choices that collectively bias results toward statistical significance. Should we winsorise outliers? At the 95th or 99th percentile? Should we include or exclude penny stocks? What lag structure should we use? Each choice seems reasonable in isolation, but the researcher who tries multiple specifications and reports the one that "works" has effectively searched across many analyses without accounting for this search in the final inference.

Publication bias amplifies these problems. When journals and prestigious conferences favour statistically significant results, the published literature systematically overstates effect sizes. A strategy that appears to work in one published study may simply represent the lucky draw from many attempted analyses, most of which failed to achieve significance and therefore went unpublished. Meta-analyses consistently show that published effect sizes shrink dramatically when studies with null findings are included, suggesting that what we see in top journals is often the tip of an iceberg where the bulk of contradictory evidence remains hidden.

::: {.callout-tip}

## A Better Approach

Report effect sizes and confidence intervals rather than focusing on p-values and significance tests. Ask "Is this effect large enough to matter economically?" rather than "Is p < 0.05?" When comparing strategies or groups, test the difference directly rather than comparing individual significance tests. And recognise that statistical significance, while providing information about sampling variability, says little about practical importance, causation, or replicability.

:::

## Regression Analysis: Estimation, Interpretation, and the Assumptions That Actually Matter

Regression analysis estimates relationships between variables, providing the workhorse tool of both classical econometrics and modern data science. In its simplest form, we model an outcome $Y$ as a linear function of predictors $X$:

$$Y_i = \beta_0 + \beta_1 X_{1i} + \beta_2 X_{2i} + \cdots + \beta_k X_{ki} + \varepsilon_i$$

Ordinary Least Squares (OLS) estimation finds the coefficients that minimise the sum of squared residuals: $\hat{\boldsymbol{\beta}} = (\mathbf{X}'\mathbf{X})^{-1}\mathbf{X}'\mathbf{Y}$. Under the Classical Linear Regression Model (CLRM) assumptions, OLS estimators are BLUE : Best Linear Unbiased Estimators. These assumptions include linearity of the relationship in parameters, strict exogeneity ($\mathbb{E}[\varepsilon_i | \mathbf{X}] = 0$), no perfect multicollinearity among predictors, homoscedasticity (constant error variance), and no autocorrelation in the errors. When these assumptions hold, inference becomes straightforward: we can use t-tests for individual coefficients, F-tests for joint significance, and R² as a measure of goodness of fit. The Gauss-Markov theorem guarantees that under these conditions, OLS achieves minimum variance among all linear unbiased estimators.

But which of these assumptions actually matter most in practice? Traditional textbooks present regression assumptions in mathematical order, which @gelman2020regression argue obscures what practitioners should worry about. Their ranking by *importance* reorders our priorities:

| Rank | Assumption | Why It Matters |

|:----:|------------|----------------|

| 1 | **Validity** | Does your model address your research question? Are you measuring what you think you're measuring? |

| 2 | **Representativeness** | Is your sample representative of the population you want to study? |

| 3 | **Additivity & Linearity** | The most important *mathematical* assumption : is the true relationship linear? |

| 4 | **Independence of errors** | Violated in time series, spatial, and multilevel settings |

| 5 | **Equal variance** | Heteroscedasticity rarely affects conclusions substantively |

| 6 | **Normality of errors** | "Barely important at all" for estimation : only matters for prediction intervals |

: Regression Assumptions in Order of Importance (Gelman, Hill & Vehtari, 2020) {#tbl-assumptions-ranked}

Most econometrics training focuses intensively on assumptions three through six : the mathematical conditions that determine when OLS is BLUE. We learn to test for heteroscedasticity, check for autocorrelation, worry about multicollinearity, and verify that errors follow a normal distribution. But Gelman argues that **validity** and **representativeness** : which are harder to test with formal diagnostics : matter far more in practice. A perfectly estimated regression on the wrong data, or on an unrepresentative sample, answers the wrong question no matter how beautifully it satisfies the Gauss-Markov conditions. Does your model actually address the research question you care about? Are you measuring the constructs you think you are measuring? Is your sample representative of the population you want to understand? These questions require domain knowledge and careful thought about the data-generating process, not just diagnostic tests on residuals.

::: {.callout-warning}

## Where Attention Should Focus

The assumptions that receive the most attention in econometrics courses (normality of errors, homoscedasticity) are often the least consequential, while validity and representativeness : which resist formal testing : matter most for whether your analysis provides useful answers. A technically perfect analysis of unrepresentative data is worse than useless; it provides false confidence.

:::

The BLUE property itself deserves clarification. "Best" means OLS achieves minimum variance among all linear unbiased estimators : no other unbiased estimator that is a linear function of the data can be more precise. "Linear" means the estimator $\hat{\beta}$ is a linear function of the dependent variable $Y$. "Unbiased" means that $\mathbb{E}[\hat{\beta}] = \beta$ : on average across repeated samples, our estimates hit the true value. The Gauss-Markov theorem guarantees BLUE under the five classical assumptions, but crucially, if we care only about unbiasedness rather than minimum variance, we can relax some assumptions. This distinction matters for understanding when and how OLS fails, and for recognising that biased estimators (like ridge regression or lasso) can sometimes outperform OLS by accepting a small amount of bias in exchange for substantial variance reduction.

## What Regression Coefficients Actually Tell Us

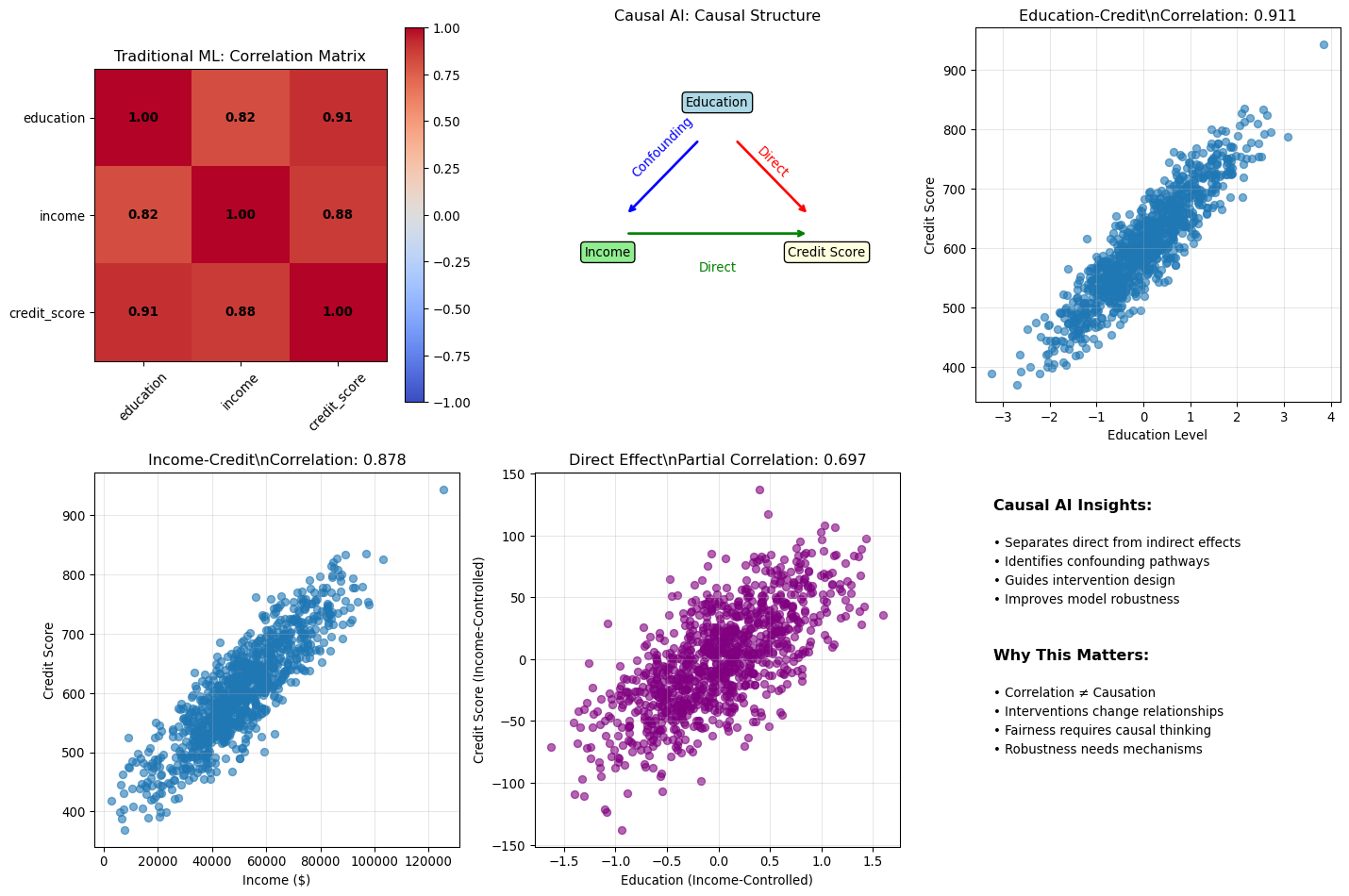

Regression coefficients are commonly called "effects," but @gelman2020regression argue this terminology is misleading and leads to serious interpretive errors. Consider a regression estimating the relationship between ESG scores and stock returns from cross-sectional data: `annual_return = 8.2 + 0.15 × ESG_score + 0.02 × market_cap + error`. The coefficient 0.15 might be reported as "the effect of ESG is 15 basis points per unit score," but this language is dangerously imprecise. What we actually observe is a **comparison**: companies with higher ESG scores have, on average, higher returns than otherwise similar companies in our sample. This is a pattern in the data : a between-firm comparison. To claim an "effect" implies something stronger: that if we took a company and increased its ESG score by one unit, its returns would increase by 15 basis points. This describes a hypothetical within-firm intervention that our observational cross-sectional data cannot possibly support.

Why does this distinction matter beyond mere semantics? High-ESG companies may differ systematically from low-ESG companies in ways we have not measured : better management quality, stronger governance structures, more patient investors, different risk profiles. The observed return difference could reflect these omitted factors rather than ESG practices themselves. If a company adopted ESG practices *only* to boost returns, without these other characteristics, the 15 basis point "effect" might not materialise at all. The language of "effects" invites causal interpretation that the research design cannot support.

::: {.callout-note}

## Getting the Language Right

- **Comparison (what we observe)**: "Firms with ESG scores one point higher have returns 15bp higher on average, controlling for market capitalisation"

- **Effect (a causal claim)**: "Improving ESG by one point *causes* returns to increase by 15bp"

The first describes an association in the data; the second makes a causal claim that requires additional evidence beyond observational regression. Always ask: are we describing a between-unit comparison, or claiming a within-unit effect?

:::

This issue pervades finance research. Consider three more examples: a coefficient of 0.3 on analyst coverage tells us that firms with more coverage have higher returns (comparison), not that adding analysts causes higher returns (effect). A coefficient of -0.05 on leverage indicates that more leveraged firms earn lower returns (comparison), not that reducing leverage increases returns (effect). A coefficient of 0.02 on insider ownership shows that higher ownership associates with better performance (comparison), not that giving managers more shares improves performance (effect). In each case, the regression tells us about associations between firms that differ on these dimensions. Whether *changing* these characteristics would *cause* the predicted outcome requires different evidence: randomised experiments, instrumental variables, regression discontinuity designs, or careful natural experiments. The comparative interpretation is always available from regression coefficients; the causal interpretation requires additional assumptions and research design choices.

## Regression to the Mean, the Limits of R², and the Difficulty of Interactions

The phenomenon of "regression to the mean" : Galton's original discovery that gave regression analysis its name : has profound implications for interpreting patterns in financial data. Children of very tall parents tend to be tall, but *less tall than their parents* on average. Children of very short parents tend to be short, but *less short than their parents*. Heights "regress" toward the population average not because of any biological force, but because extreme observations typically contain both signal (true underlying value) and luck (random variation). On repeated measurement, the luck component averages out, pulling observations toward the mean. In finance, this manifests in performance persistence: last year's top-performing fund managers will, on average, perform closer to the mean next year : not necessarily because their skill deteriorated, but because their exceptional year likely contained some luck alongside skill. Extreme P/E ratios tend to normalise over time. Unusually high or low earnings growth rates typically moderate. Mistaking regression to the mean for a causal effect is one of the most common errors in practical analysis. When a company that performed poorly last year improves this year, did the new CEO cause the improvement, or would regression to the mean have produced similar results anyway? Distinguishing these scenarios requires careful thought about counterfactuals, not just observing that performance changed.

::: {.callout-warning}

## The Regression Fallacy

Regression to the mean creates patterns that look like causal effects but reflect pure statistical artifacts. Before attributing performance changes to interventions, consider whether random variation around a stable mean could explain the observed pattern. This is especially important in "before-after" comparisons without proper control groups.

:::

Understanding R² requires similar care in interpretation. The coefficient of determination measures the proportion of variance explained: $R^2 = 1 - \frac{\sum(y_i - \hat{y}_i)^2}{\sum(y_i - \bar{y})^2}$. @gelman2020regression make the useful point that a model predicting earnings from height and sex yields R² ≈ 0.10, meaning 90% of earnings variation has nothing to do with these predictors. Yet the regression remains informative : it reveals a genuine association, even though it cannot predict individual outcomes with much precision. R² tells us how much variance our predictors explain and whether adding variables improves explanatory power, but it does *not* tell us whether the model is correct (a misspecified model can have high R²), whether the model is useful for decision-making (low R² can still be economically significant), or whether the relationships are causal (R² says nothing about causation). In finance, R² values of 0.01-0.05 are common when predicting returns, reflecting the fundamental difficulty of forecasting prices rather than necessarily indicating model failure. Signal-to-noise ratios are inherently low in financial markets : if prediction were easy, arbitrage would eliminate the opportunity.

A final subtlety concerns interaction effects. @gelman2020regression document a crucial but often overlooked fact: **estimating interaction effects requires roughly four times the sample size of estimating main effects** at the same level of precision. Why? The standard error of an interaction is approximately twice the standard error of the main effect, so achieving the same precision requires quadrupling the sample size. This has immediate implications for finance research: a study powered to detect a "size effect" will typically be underpowered to detect whether that effect varies across industries. If you find a statistically significant interaction in an exploratory analysis, it is likely overestimated due to selection bias : what Gelman calls the "winner's curse" of interactions. When you design a study to detect a main effect and then explore interactions, statistically significant interactions will on average overestimate the true effect by a factor of about 2.6, because you are selecting the largest observed differences from a noisy distribution. Designing studies to detect varying effects (such as "does momentum work differently in bull versus bear markets?") requires substantially more data than detecting average effects, a reality that many published interaction findings conveniently ignore.

## When Assumptions Fail: Consequences and Remedies

Financial data routinely violates CLRM assumptions, so recognising these violations and understanding their consequences becomes essential for responsible inference. Heteroscedasticity : non-constant error variance : is ubiquitous in finance. Volatility clustering means high-volatility periods follow high-volatility periods, violating the constant-variance assumption. The good news: OLS coefficient estimates remain unbiased. The bad news: standard errors are incorrect, invalidating hypothesis tests and confidence intervals. Remedies include robust (Huber-White) standard errors that remain valid under heteroscedasticity, weighted least squares when the variance structure is known, or GARCH models that explicitly model time-varying volatility.

Autocorrelation : correlated errors : appears in nearly all time series data. Yesterday's forecast error predicts today's, violating the independence assumption. OLS remains unbiased, but standard errors are incorrect and typically *understated*, leading to inflated t-statistics and false confidence in rejecting null hypotheses. Newey-West (heteroscedasticity and autocorrelation consistent) standard errors provide one remedy, along with generalised least squares or explicit time series models that incorporate the serial dependence directly. Multicollinearity : highly correlated predictors : is common when using many factors simultaneously. OLS remains unbiased and standard errors remain valid, but variance explodes, making estimates unstable and imprecise. Variable selection, principal components, or regularisation methods like ridge regression offer paths forward.

Endogeneity : correlation between predictors and errors : represents the most serious violation because it renders OLS both biased and inconsistent. If $\text{Cov}(X, \varepsilon) \neq 0$, increasing the sample size will not fix the problem; the bias persists asymptotically. This violation arises from omitted variables, measurement error, or simultaneity, and requires fundamentally different identification strategies: instrumental variables, difference-in-differences, or regression discontinuity designs. The table below summarises the consequences of each violation and available remedies:

| Violation | OLS Unbiased? | OLS BLUE? | Standard Errors Valid? | Remedy |

|-----------|:-------------:|:---------:|:----------------------:|--------|

| Heteroscedasticity | ✓ | ✗ | ✗ | White (HC) SEs |

| Autocorrelation | ✓ | ✗ | ✗ | Newey-West (HAC) |

| Multicollinearity | ✓ | ✓ | ✓ (but imprecise) | Regularisation |

| Endogeneity | ✗ | ✗ | ✗ | IV methods |

: Summary of Assumption Violations and Their Consequences {#tbl-violations}

::: {.callout-important}

## The Path to Machine Learning

Understanding assumption violations provides a natural bridge to machine learning methods. Regularisation techniques like ridge regression and lasso directly address multicollinearity by adding penalty terms that shrink coefficients. Tree-based methods handle nonlinearity and interactions automatically without requiring explicit specification. Sequence learning models explicitly account for temporal dependencies. These are not departures from econometrics : they are principled extensions that relax restrictive assumptions when data patterns demand it.

:::

## Extending to Binary Outcomes: Logistic Regression and the Divide-by-4 Rule

Many financial questions involve binary outcomes rather than continuous variables: Will this loan default? Will this stock beat the market? Will this trade be profitable? Logistic regression extends the regression framework to these settings by modelling the *probability* of the positive class rather than predicting a continuous outcome directly:

$$\text{Pr}(Y=1 | X) = \text{logit}^{-1}(\beta_0 + \beta_1 X_1 + \cdots) = \frac{1}{1 + e^{-(\beta_0 + \beta_1 X_1 + \cdots)}}$$

The logistic transformation ensures that predicted probabilities remain bounded between zero and one, but it creates an interpretation challenge: coefficients are notoriously difficult to understand because of the nonlinear relationship. @gelman2020regression offer a practical heuristic: **divide the coefficient by 4** to get an upper bound on the change in probability for a one-unit change in the predictor. This works because the logistic curve is steepest at its centre, where the probability equals 0.5, and at that point the slope equals $\beta/4$. Dividing by 4 therefore gives the *maximum* possible effect on probability.

As a concrete example, if a logistic regression predicting loan default yields a coefficient of 0.4 for debt-to-income ratio, then a one-unit increase in debt-to-income corresponds to *at most* a 10 percentage point increase in default probability (0.4 ÷ 4 = 0.10). This approximation works best when baseline probabilities are near 50%; for rare events like bankruptcy or fraud, the actual probability change will be smaller than $\beta/4$. When precision matters, compute exact predicted probabilities or use simulation rather than relying on this heuristic.

## Testing Your Methods with Fake Data

Before trusting results from real data, @gelman2020regression advocate **fake-data simulation** as an essential validation step: generate synthetic data from a known process, apply your analysis procedure, and check whether you recover the true parameters. The workflow is straightforward. First, specify a data-generating process with known parameters : for instance, returns following a factor model with a known alpha. Second, simulate data from this process. Third, apply your estimation procedure exactly as you would to real data. Fourth, compare your estimates to the true values you built into the simulation. Fifth, repeat this process many times to assess the variability of your estimates and understand how often your procedure succeeds or fails.

Why does this matter in finance? Fake-data simulation lets you test whether your backtesting methodology can detect a strategy that *actually* works, rather than just finding spurious patterns. It verifies that your standard errors are correct under controlled conditions before you apply them to messy real data. It helps you understand the distribution of test statistics under the null hypothesis, which is crucial for interpreting p-values. And it calibrates your expectations for what can be learned from your sample size : if you cannot detect a 1% alpha with 10 years of daily data in simulations where that alpha truly exists, you have no business claiming to have found one in real data. The logic is simple but powerful: if your procedure cannot recover known effects from fake data, it cannot be trusted with real data where the truth is unknown.

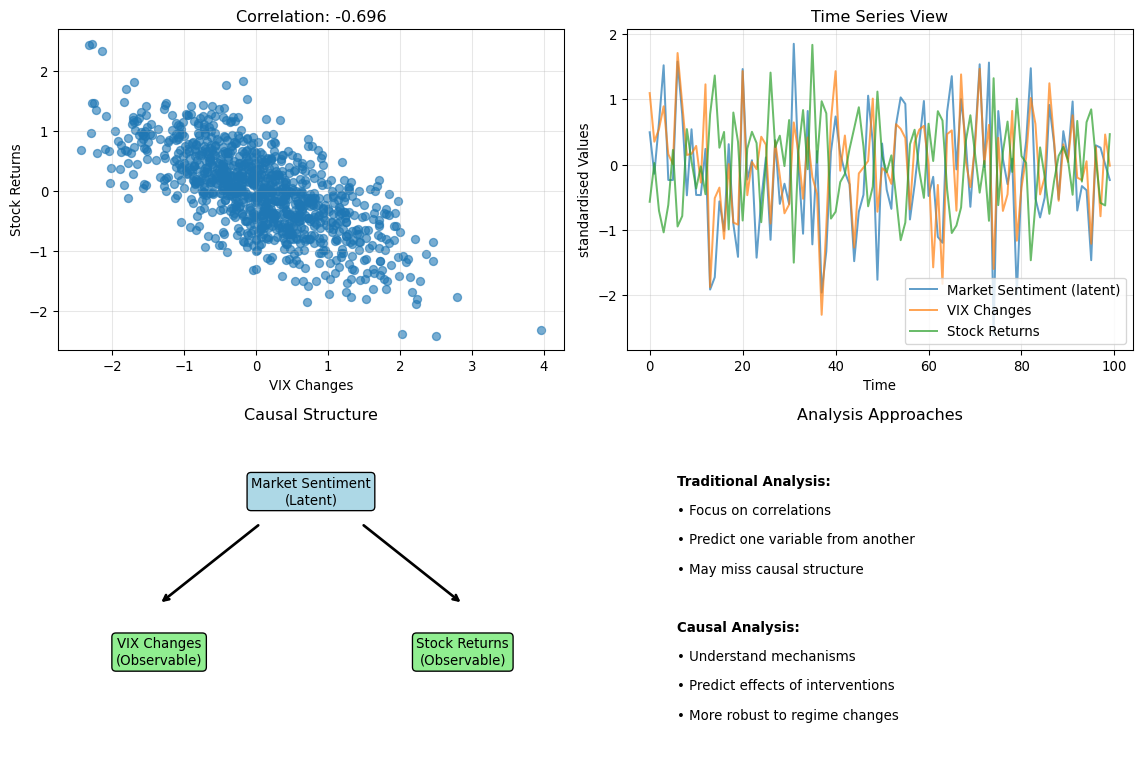

## Thinking Causally: When Can Regression Support Causal Claims?

The distinction between prediction and causation is fundamental, yet routinely ignored in finance. @gelman2020regression provide a rigorous framework for thinking carefully about when we can : and cannot : make causal claims from observational data. Causal effects are defined as comparisons between *potential outcomes* under different scenarios. For a treatment $z$ (such as receiving investment advice), each unit $i$ has two potential outcomes: $y_i^0$ (the outcome if untreated) and $y_i^1$ (the outcome if treated). The **individual causal effect** is $y_i^1 - y_i^0$. The fundamental problem of causal inference is that we can only ever observe *one* of these potential outcomes for each unit : the counterfactual is never observed. Did a new risk management system reduce losses? We observe losses with the system ($y^1$) but never observe what losses would have been without it ($y^0$). Any comparison requires untestable assumptions about this unobserved counterfactual.

To estimate causal effects from observational data, we typically invoke the **ignorability** (or "selection on observables") assumption: conditional on observed covariates $x$, treatment assignment is independent of potential outcomes, $y^0, y^1 \perp z | x$. In finance terms, this means that after controlling for everything we measure, the decision to adopt a strategy is unrelated to what outcomes would have been. This is a strong assumption that fails when firms adopt strategies *because* they expect better outcomes (selection bias), when unmeasured factors affect both the treatment decision and outcomes (confounding), or when adoption timing correlates with market conditions. Ignorability cannot be tested directly : it is an assumption about unobserved potential outcomes. We can check balance on observed covariates, but balance on observables does not guarantee balance on unobservables.

::: {.callout-warning}

## Common Causal Errors in Finance

Three errors appear repeatedly. First, adjusting for post-treatment variables that are *affected by* the treatment biases estimates, even in randomised experiments : if studying whether ESG adoption affects returns, do not control for media coverage that follows ESG adoption, as it is part of the causal pathway. Second, confusing correlation with causation leads to unwarranted conclusions : a regression of returns on analyst coverage estimates a comparison, not a causal effect, since companies that attract coverage differ systematically from those that do not. Third, selection on the dependent variable, such as studying only successful funds to learn "what works," ignores all the funds that tried the same strategies and failed, introducing severe survivorship bias.

:::

When ignorability fails, **instrumental variables (IV)** offer one potential escape route. An instrument $z$ must satisfy three conditions: relevance ($z$ affects treatment assignment), exclusion restriction ($z$ affects outcomes *only through* its effect on treatment), and independence ($z$ is as-good-as-randomly assigned). The IV estimate captures the causal effect for **compliers** : units whose treatment status was actually changed by the instrument. Finance applications include using regulatory changes as instruments for capital structure decisions, geographic distance as an instrument for analyst coverage, or lottery-based assignment to index inclusion. As @gelman2020regression advise, do not try to extract causal conclusions from large regressions with many controls. Instead, design your analysis around a specific causal question with a credible identification strategy that makes the necessary assumptions explicit and defensible.

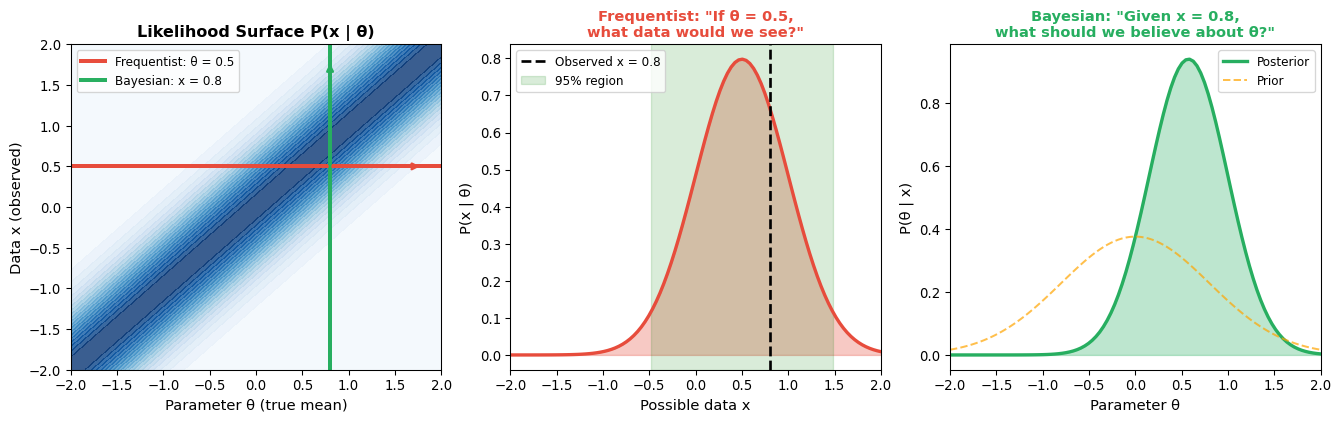

## Bayesian Inference as Information Combination

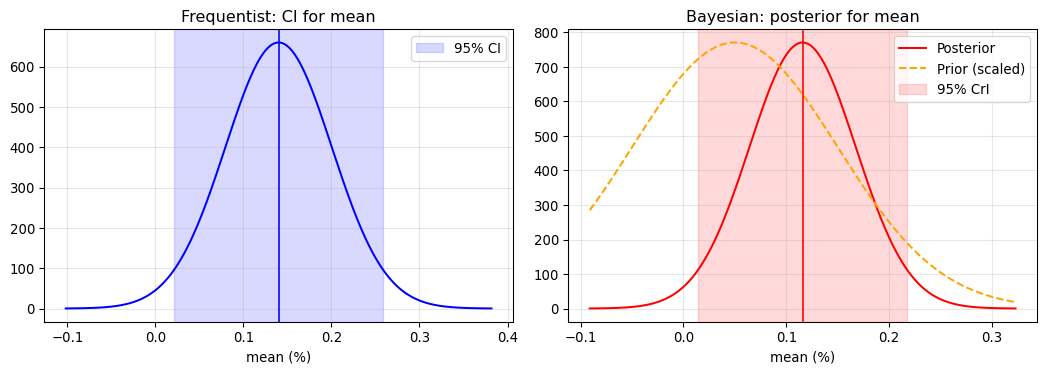

Frequentist inference treats parameters as fixed unknown quantities and data as random draws from a distribution. Bayesian inference inverts this perspective: parameters are treated as random variables with probability distributions, and we update our beliefs as data arrive. The core formula, $\text{Posterior} \propto \text{Likelihood} \times \text{Prior}$, combines prior beliefs with new evidence in a mathematically principled way. For a parameter $\theta$ with prior estimate $\hat{\theta}_{\text{prior}}$ (standard error $\text{se}_{\text{prior}}$) and data estimate $\hat{\theta}_{\text{data}}$ (standard error $\text{se}_{\text{data}}$), the Bayesian posterior estimate emerges as a weighted average: $\hat{\theta}_{\text{Bayes}} = \frac{\hat{\theta}_{\text{prior}}/\text{se}_{\text{prior}}^2 + \hat{\theta}_{\text{data}}/\text{se}_{\text{data}}^2}{1/\text{se}_{\text{prior}}^2 + 1/\text{se}_{\text{data}}^2}$. Each source of information is weighted by its precision (inverse variance). When prior and data have equal precision, the Bayesian estimate sits at their midpoint; otherwise, it is pulled toward whichever source is more precise. This provides a principled way to combine historical data with economic theory, shrink extreme estimates toward reasonable values, or incorporate expert judgment formally rather than informally.

@gelman2020regression advocate **weakly informative priors** : not so strong as to dominate the data, but informative enough to rule out implausible values (such as Sharpe ratios of 10), stabilise estimates when data are sparse, and provide regularisation similar to ridge regression. The default prior in Bayesian regression software like `stan_glm` typically centres coefficients at zero with standard deviation scaled to the data, creating a gentle pull toward "no effect" that prevents overfitting. When does the prior matter? With large samples and strong signal, the data overwhelm the prior and frequentist and Bayesian answers converge. With small samples and weak signal, the prior provides regularisation and estimates shrink toward prior values. When prior and data contradict each other, the posterior represents a compromise weighted by relative precision. In finance, priors matter most when estimating returns with short samples (where priors on expected Sharpe ratios matter), working with rare events like fraud or default where data are sparse, or combining multiple noisy signals into a single estimate.

::: {.callout-tip}

## A Pragmatic View

Even if you are philosophically frequentist, Bayesian methods can be useful computationally (MCMC enables fitting complex models) and practically (regularisation, combining evidence). The methods often give similar answers when sample sizes are large : the real benefit is forcing explicit thought about prior information and how it should combine with data.

:::

::: {.callout-note}

## Applied Example: Signal-to-Noise in Financial Returns

A concrete illustration of Bayesian uncertainty quantification comes from measuring **return predictability**. How much of daily return variance is predictable from past returns? We can answer this by fitting a Bayesian AR(1) model and examining the posterior distribution of R² = ρ² (the squared autocorrelation).

For S&P 500 (SPY) daily returns, a Bayesian bootstrap analysis yields:

- **Posterior median R²**: 1.66%

- **95% credible interval**: [0.08%, 6.24%]

The credible interval is wide: but this width is itself deeply informative. We cannot even precisely measure how little predictability there is because the signal is so weak relative to noise. Consider what the interval tells us:

| Scenario | R² | Noise fraction |

|----------|-----|---------------|

| Pessimistic (lower bound) | 0.08% | 99.92% |

| Median | 1.66% | 98.34% |

| Optimistic (upper bound) | 6.24% | 93.76% |

Even at the optimistic upper bound, over 93% of variance is unpredictable noise. The wide interval does not undermine the conclusion: it reinforces it. A point estimate alone (R² = 1.66%) would hide this uncertainty; the posterior distribution reveals the fundamental difficulty of financial inference.

This is exactly when Bayesian thinking adds value: when signal is weak, samples are noisy, and honest uncertainty quantification matters more than false precision.

:::

One of the most practically valuable Bayesian concepts is **partial pooling**, which provides a principled middle ground between complete pooling (treating all groups as identical, ignoring real differences) and no pooling (estimating each group separately, yielding noisy estimates with small samples). As @gelman2006data explain, "Both these approaches have problems: no pooling ignores information and can give unacceptably variable inferences, and complete pooling suppresses variation that can be important." Consider estimating expected returns for 50 industry portfolios using only 5 years of monthly data per industry. No pooling means estimating each industry mean separately, but small samples produce noisy estimates where extreme values likely reflect chance rather than signal. Complete pooling means using the overall market return for all industries, ignoring valuable information that industries differ. Partial pooling estimates a hierarchical model where industry means are drawn from a common distribution, shrinking extreme estimates toward the grand mean while allowing well-estimated means to stay closer to their data. This shrinkage is automatic and data-driven: industries with noisier data shrink more, industries with clearer signals shrink less. This formalises what a sensible analyst would do informally.

::: {.callout-important}

## Shrinkage is Regularisation

Partial pooling and ridge regression achieve similar goals through different routes. Ridge regression adds a penalty term $\lambda \sum \beta_j^2$ to the loss function, shrinking coefficients toward zero. Partial pooling places a normal prior $\beta_j \sim N(0, \sigma^2_\beta)$ on coefficients, also shrinking toward zero (or a common mean). The Bayesian approach has the advantage of automatically learning the appropriate amount of shrinkage from the data rather than requiring manual tuning of a penalty parameter.

:::

Partial pooling matters most in settings common to finance: cross-sectional asset pricing where we estimate firm-level betas with limited time series, fund performance evaluation where we separate skill from luck across many funds, risk forecasting where we combine individual asset volatilities with market-wide information, and portfolio optimisation where we shrink sample covariance matrices toward structured targets. The James-Stein estimator : which showed that shrinking sample means toward a common value improves *total* estimation accuracy : is a frequentist result that has a natural Bayesian interpretation through hierarchical models, demonstrating that these perspectives can converge on practical recommendations despite their philosophical differences.

## Model Selection Without Overfitting: Cross-Validation and Information Criteria

Choosing among competing models is one of the most consequential decisions in applied work, yet the natural approach : comparing performance on the data used for estimation : is fundamentally flawed. @efron2016casi trace two major approaches that address this problem: cross-validation (developed in the 1970s) and information criteria (emerging with Mallows' $C_p$ and AIC). When we fit a model to training data and evaluate its performance on those *same* data, we obtain the **apparent error**, which is optimistically biased because the model has seen these observations during estimation. What we actually care about is the **true error**: how well will the model predict *new* data drawn from the same distribution? The gap between apparent and true error grows with model complexity, since more parameters provide more opportunity to fit noise rather than signal.

Cross-validation addresses this by systematically holding out data during estimation and evaluating on those held-out observations. Leave-one-out (LOO) cross-validation fits $n$ models, each excluding one observation, then averages prediction error across all held-out points : this has low bias but high variance. K-fold cross-validation partitions data into $K$ groups, rotating which group is held out, balancing bias and variance. Time-series cross-validation uses rolling or expanding windows and crucially never trains on future data to predict past observations, respecting temporal dependence. As @gelman2020regression explain, "Cross validation... avoids some of the problems of overfitting. The simplest version is the leave-one-out approach, in which the model is fit $n$ times, in each case excluding one data point."

::: {.callout-important}

## Time Structure Matters

Standard K-fold cross-validation assumes observations are exchangeable and can be randomly shuffled. In finance, time series structure means this assumption fails catastrophically : using future returns to predict past returns is not validation, it is cheating. Always use time-aware cross-validation where the test set is strictly *after* the training set, simulating realistic forecasting conditions.

:::

An alternative to cross-validation estimates prediction error analytically by adding a complexity penalty to training error: $\text{Estimated Prediction Error} = \text{Training Error} + \text{Penalty}(k, n)$. Common criteria include AIC (penalty $2k$, asymptotically equivalent to LOO-CV), BIC (penalty $k \ln(n)$, stronger penalty favoring simpler models), Mallows' $C_p$ (penalty $2k\hat{\sigma}^2$ for linear regression with known error variance), and WAIC (Bayesian criterion using effective number of parameters that generalises to complex models), where $k$ denotes the number of parameters and $n$ the sample size. AIC and cross-validation answer slightly different questions: AIC estimates expected log-likelihood on new data (a measure of fit or calibration), while LOO-CV estimates expected squared prediction error (a measure of point-prediction accuracy). For most purposes they rank models similarly, but the distinction matters when you care about probabilistic calibration versus point prediction.

What does this mean in practice for finance? First, use time-series cross-validation for return prediction, never allowing information to leak from future to past : rolling windows simulate real-time forecasting and reveal how models degrade as market conditions change. Second, maintain appropriate scepticism about in-sample fit: a model with $R^2 = 0.90$ on training data may achieve $R^2 \approx 0$ out-of-sample, especially with many predictors where overfitting becomes severe. Third, recognise that BIC's stronger penalty helps identify the "true" model (if one exists) while AIC optimises predictive accuracy even if it includes some noise variables, so prefer BIC for model identification and AIC for prediction tasks. Fourth, watch for multiple testing: if you try 100 models and select the best by cross-validation, your reported CV error is optimistically biased because you have searched across many specifications. The more you search, the more conservative your assessment of final model performance should be.

::: {.callout-tip}

## Hierarchy of Evidence for Model Performance

Evidence quality ranges from nearly worthless to genuinely informative: In-sample $R^2$ tells you almost nothing about future performance. Information criteria (AIC, BIC) provide quick approximations but rely on asymptotic theory. Standard K-fold cross-validation improves on these but ignores time structure, making it inappropriate for financial time series. Time-series cross-validation with appropriate gaps avoids look-ahead bias and provides realistic performance estimates. True out-of-sample performance on genuinely new data : data that arrived after model specification was fixed : remains the gold standard, though in practice we rarely have the discipline to set models in stone before new data arrive.

:::

## Practical Wisdom for Applied Regression Modelling

@gelman2020regression offer practical advice that transcends the textbook treatment of regression, reflecting decades of applied experience with real problems where data are messy, assumptions fail, and the goal is insight rather than perfect adherence to mathematical conditions. Their recommendations reshape how we should approach statistical modelling in finance, moving from mechanical application of procedures toward thoughtful, iterative analysis.

Perhaps the most fundamental insight concerns how we think about uncertainty. Variation across datasets matters more than standard errors from a single study : if you fit the same model to different samples, coefficients will vary, and understanding this variation is often more useful for applications than obsessing over standard errors from one particular analysis. In finance, this means reporting how findings change across subperiods and across markets, which reveals robustness far more effectively than any single p-value from one time period. This connects to a second recommendation: abandon the p < 0.05 threshold as a decision rule. The arbitrary distinction between p = 0.049 and p = 0.051 throws away information, and in finance where everything affects everything to some degree, true zeroes do not exist : factor returns are not exactly zero, correlations are not exactly zero, and whether a confidence interval excludes zero tells you little about future settings. Rather than asking "Is this factor significant?", ask "How large is this effect, and how much does it vary?"

Visualisation deserves more attention than diagnostics. Graph your fitted model, not just residual plots : a table of coefficients provides far less understanding than visualising what the model actually predicts, and making many graphs reveals different aspects of your data that tables conceal. What should you skip? Most of what standard packages produce automatically (Q-Q plots, influence diagrams) you will not use; focus on graphs you can explain to a skeptical audience. We discussed earlier how regression coefficients should be interpreted as comparisons between individuals rather than changes within individuals, and this comparative interpretation remains available without causal assumptions : thinking this way helps build intuition about what models actually say.

Fake-data simulation provides an essential validation step before trusting real results. Simulating data from a known process and checking whether your procedure recovers the true parameters forces you to think about realistic parameter values, reveals whether your code works correctly, and shows how precise your estimates can be given your sample size. In finance, this means simulating realistic factor returns with known alpha and asking whether your backtesting procedure can detect it : if it cannot recover known effects from fake data, your real findings may well be spurious. This connects to the recommendation to fit many models rather than searching for one "correct" specification. Start simple and add complexity gradually, recognising that working with simple models is not the research goal but rather a technique to understand what is happening before adding complications. Keep track of all models you fit to protect yourself from the "forking paths" bias that arises when you unconsciously favour specifications that produce preferred results. In finance, do not run one mega-regression; instead, build up from univariate to multivariate, from linear to nonlinear, reporting results from multiple specifications to demonstrate robustness.

Computational workflow matters more than most practitioners realise. Fast computation enables better statistics : when you can fit models quickly, you can explore more alternatives and understand your data better rather than committing to the first specification that runs. A practical strategy starts with data subsets before running on full samples, since computations on 10% of the data often reveal the same patterns as the full sample but take a fraction of the time, allowing rapid iteration. Consider transforming nearly every variable: logarithms for all-positive variables create multiplicative models appropriate for prices and returns, standardisation makes coefficients interpretable and comparable, and interactions allow effects to vary by group when you have theoretical reasons to expect heterogeneity. In finance, log returns are standard for good reasons, and standardised coefficients help compare predictors measured in different units like volatility and trading volume.

The causal inference advice we discussed earlier bears repeating: do not assume regression coefficients are causal effects, and if you want causal inference, design your analysis around that specific question rather than trying to answer multiple causal questions with one large regression : in observational data, this approach fails. Estimating "the effect of ESG on returns" requires different methods than predicting returns from ESG scores; use the right tool for each question. Finally, learn through live examples by applying methods to problems you care about, understanding your data, your measurements, and your data-collection procedures deeply enough that you know the magnitudes of your coefficients and not just their signs. This understanding proves essential for interpreting findings and catching errors that would slip past purely mechanical analysis.

::: {.callout-note}

## The Underlying Theme

These recommendations share a common insight: **statistical modelling is not mechanical procedure but thoughtful craft**. It requires judgment, iteration, and domain knowledge. The goal is not to follow a recipe but to understand your data well enough to make good decisions about specification, inference, and interpretation. Perfect adherence to textbook assumptions matters far less than understanding how violations affect your conclusions and whether your findings are robust to reasonable alternative choices.

:::

## Time Series Foundations: Stationarity, Dependence, and Long-Run Relationships {#time-series-foundations}

Financial data is inherently temporal, which means observations arrive ordered in time and potentially depend on their history in complex ways. Time series econometrics provides tools for handling this temporal structure, recognising that the independence assumption underlying cross-sectional methods breaks down when today's return depends on yesterday's volatility, or when news events create persistent effects on prices. The fundamental requirement for classical time series inference is **stationarity** : the property that a series' statistical characteristics do not change over time. Formally, a stationary series maintains constant mean ($\mathbb{E}[Y_t] = \mu$), constant variance ($\text{Var}(Y_t) = \sigma^2$), and autocovariance that depends only on lag $k$ rather than time $t$ itself: $\text{Cov}(Y_t, Y_{t-k})$ is a function of $k$ alone.

Why does stationarity matter? Because statistical inference assumes we can learn from the past to predict the future, and if the underlying process is changing : if means drift upward, if volatility regimes shift, if correlations evolve : then historical relationships may not hold going forward. The Augmented Dickey-Fuller (ADF) test evaluates whether a series has a unit root (is non-stationary) through the regression $\Delta Y_t = \alpha + \beta t + \gamma Y_{t-1} + \sum_{i=1}^{p} \delta_i \Delta Y_{t-i} + \varepsilon_t$, testing the null hypothesis $\gamma = 0$ (unit root, non-stationary) against the alternative $\gamma < 0$ (stationary). When the test statistic is sufficiently negative, below critical values that differ from standard t-distributions, we reject the null and conclude stationarity. But the ADF test has low power against near-unit-root alternatives, struggling to distinguish $\phi = 1$ from $\phi = 0.95$ especially in small samples, so failure to reject the null does not prove non-stationarity : it may simply reflect insufficient sample size to detect the difference.

::: {.callout-warning}

## Unit Root Testing in Practice

The ADF test's low power means that many financial series occupy an ambiguous zone where we cannot confidently classify them as stationary or non-stationary. This uncertainty matters for modelling choices: should we difference returns (already close to stationary) or work with levels? The answer often depends more on economic reasoning about the data-generating process than on test statistics alone.

:::

Understanding temporal dependence requires tools for measuring how observations relate to their own history. The autocorrelation function (ACF) measures correlation between a series and its lagged values: $\rho_k = \frac{\text{Cov}(Y_t, Y_{t-k})}{\text{Var}(Y_t)}$. The partial autocorrelation function (PACF) measures direct correlation at each lag while controlling for intermediate lags, isolating the unique contribution of lag $k$ after accounting for lags $1$ through $k-1$. Together, ACF and PACF guide model selection for ARIMA processes by revealing characteristic patterns: AR processes show geometric decay in ACF but sharp cutoff in PACF, while MA processes display the opposite pattern.

But here we encounter one of the most important practical lessons in financial econometrics: **the ACF of returns is typically indistinguishable from zero**. Plot the ACF of daily S&P 500 returns and you will see a flat line with all autocorrelations within the confidence bands. This is not a data quality problem or a failure of our tools: it is the empirical signature of market efficiency. Competition among traders arbitrages away predictable patterns in expected returns, leaving the conditional mean essentially unforecastable. ARIMA models, which target this conditional mean, therefore add little value for return prediction. The action is in the conditional variance (volatility clustering), which we address through GARCH models rather than ARIMA. This asymmetry: near-zero signal in the mean, substantial signal in the variance: is the organising principle for time series analysis in finance, and it explains why practitioners often find ARIMA disappointing while GARCH proves genuinely useful.

Two non-stationary series may share a common stochastic trend, moving together in the long run even as they wander in the short term. When $Y_t$ and $X_t$ are both integrated of order one (I(1)) but some linear combination $Y_t - \beta X_t$ is stationary (I(0)), the series are **cointegrated**, capturing long-run equilibrium relationships like those between spot and futures prices or related stock prices that arbitrage should keep aligned. The Engle-Granger two-step procedure estimates the cointegrating regression by OLS ($Y_t = \beta_0 + \beta_1 X_t + u_t$) and then tests whether the residuals $\hat{u}_t$ are stationary using a modified ADF test with different critical values to account for the fact that residuals come from an estimated relationship rather than raw data. If the residuals are stationary, the variables are cointegrated, suggesting a mean-reverting spread that provides the foundation for pairs trading strategies, tests of price discovery between spot and futures markets, and evaluations of the expectations hypothesis across the yield curve.

::: {.callout-tip}

## Connecting Classical and Modern Approaches

Classical time series methods assume you can transform data to stationarity through differencing, detrending, or other transformations. Modern sequence learning approaches like LSTMs and Transformers can learn directly from non-stationary sequences by capturing patterns in how the data evolves over time, including regime changes and structural breaks that violate stationarity. This represents one bridge from the classical foundations in Part 0 to the machine learning extensions in later chapters, showing how newer methods relax restrictive assumptions when data patterns demand it.

:::

---

# Part I: The Complexity Paradox in Financial Data Science

In finance we rarely ask whether a model is “true”. We ask whether it is useful out of sample, robust to changing conditions, and interpretable enough to trust. That makes model complexity : how many parameters, interactions, and non‑linearities we allow : a practical decision rather than a slogan about “simplicity”.

Recent research by @kelly2024complexity challenges one of the most fundamental assumptions in statistical modelling. Contrary to conventional wisdom that often favours "simple" models with few parameters, Kelly, Malamud, and Zhou demonstrate that in the specific setting of return prediction, high‑dimensional "complex" models: where the number of parameters can exceed the number of observations: may outperform simple ones. This result establishes the rationale for modelling expected returns with machine learning techniques, but it should not be taken as a blanket endorsement of complexity.

The lesson is more nuanced. As @mcelreath2020statistical stresses, "Occam's razor is a folk heuristic; information theory is not." While Occam's razor suggests we should prefer simpler explanations, information theory provides us with mathematical tools to make this trade-off more precise.

In practice, model comparison is an out-of-sample question. If you only evaluate fit on the data used for training, more flexible models will usually look better : partly because they are learning noise. Information criteria (AIC/BIC/WAIC) formalise this by penalising complexity, and cross-validation formalises it by evaluating on held-out data. We return to this explicitly in the “Model Selection and Validation” section below. @kennedy2008econometrics gives the applied rule of thumb: keep models “sensibly simple” : complex enough to capture important features, but not more complicated than needed.

Taken together, these perspectives highlight that modern financial markets may indeed demand complex, high‑dimensional models. Yet the virtue of complexity is conditional: models must be validated, regularised, and compared against simpler alternatives. The art of financial data science is knowing when complexity adds genuine insight and when it merely overfits noise.

Yet this embrace of complexity must be balanced with intellectual humility. As @box1987empirical famously observed, “All models are wrong, but some are useful” (Box & Draper, *Empirical Model‑Building and Response Surfaces*, 1987, p. 424). The challenge in modern financial data science is building sophisticated models that are both complex enough to capture important patterns and robust enough to avoid overfitting to noise.

# Part II: The Bias-Variance Tradeoff {#sec-bias-variance}

## The Tradeoff in Financial Context

The tension between simple and complex models reflects one of the most fundamental concepts in statistical learning: the bias-variance tradeoff. Understanding this tradeoff is crucial for financial applications because it helps us think systematically about when more sophisticated methods are likely to be beneficial.

### Understanding Bias and Variance

To appreciate why the @kelly2024complexity findings are so significant, we need to understand what bias and variance actually represent in the context of model performance. These concepts, while abstract, have very concrete implications for financial decision-making.

Bias represents the systematic error in our model's predictions: the extent to which our model consistently misses the true underlying relationship. A high-bias model is like a marksman whose shots consistently land to the left of the target. No matter how many times they shoot, the pattern of misses remains the same. In financial terms, a high-bias model might consistently underestimate the volatility of certain assets or fail to capture important nonlinear relationships in market data.

Variance captures how much our model's predictions fluctuate when trained on different samples of data. A high-variance model is like a marksman whose shots are scattered widely around the target: sometimes hitting the bullseye, sometimes missing completely. In financial applications, high-variance models are particularly dangerous because they can lead to overfitting, where the model memorises the specific patterns in our training data but fails to generalise to new market conditions.

The mathematical relationship between these concepts is elegantly captured in the bias-variance decomposition. For any prediction model, the expected squared error can be decomposed as:

::: {.callout-note}

#### Bias–Variance Decomposition (squared error)

For squared loss at a fixed input $x$, with true regression function $f^*(x)=\mathbb E[Y\mid X=x]$ and noise $\varepsilon=Y-f^*(X)$:

$$

\mathbb E\big[(Y-\hat f(x))^2\big]

\;=\; \underbrace{\big(\mathbb E[\hat f(x)]-f^*(x)\big)^2}_{\text{Bias}^2(x)}

\;+\; \underbrace{\operatorname{Var}(\hat f(x))}_{\text{Variance}(x)}

\;+\; \underbrace{\operatorname{Var}(\varepsilon\mid X=x)}_{\text{Irreducible error}}.

$$

- Bias$^2(x)$: systematic gap between the average fitted model and the truth.

- Variance$(x)$: spread of the fitted model across training samples (sensitivity to data).

- Irreducible error: conditional noise in the data‑generating process; even a perfect model cannot beat this term.

In finance, heteroskedasticity (time‑varying volatility) means $\operatorname{Var}(\varepsilon\mid X=x)$ often depends on $x$ and time; non‑stationarity means that some “variance” reflects drift in $f^*(x)$.

The practical takeaway: consistent with @efron2016casi: is that lowering bias via more complex models only helps out‑of‑sample when the induced variance doesn’t dominate. See @hilpisch2019 for squared‑loss implementations and diagnostics in Python (curated, commit‑pinned links: resources/hilpisch-code.qmd).

:::

This decomposition reveals why the tradeoff is so fundamental: reducing bias typically increases variance, and vice versa. The irreducible error represents the inherent noise in the data that no model can eliminate.

The practical implication, as @murphy2012machine puts it: "it might be wise to use a biased estimator, so long as it reduces our variance, assuming our goal is to minimise squared error." This is precisely why regularisation methods like ridge regression deliberately introduce bias : the variance reduction more than compensates, leading to better predictions on new data.

### The Traditional Wisdom and Its Limitations

Traditional statistical wisdom, rooted in classical inference theory as described in @efron2016casi, suggests that simpler models are generally preferable because they have lower variance: they're less likely to overfit to the specific sample of data we happen to observe. This wisdom emerged from an era when data was scarce and computational resources were limited, making the stability of simple models particularly valuable.

The classical approach, as Efron and Hastie note, was designed for "small data sets, often a few hundred numbers or fewer, laboriously collected by individual scientists working under restrictive experimental constraints." In this context, the bias-variance tradeoff typically favoured simpler models because the variance penalty of complex models was too high relative to the available data.

However, @kelly2024complexity demonstrate that in modern financial applications, this traditional wisdom can be misleading. The bias reduction from using more complex models can outweigh the variance increase, leading to better out-of-sample performance. This finding suggests that the financial domain may have characteristics that make the bias-variance tradeoff behave differently than in traditional statistical applications.

### Stylised Facts about Financial Data

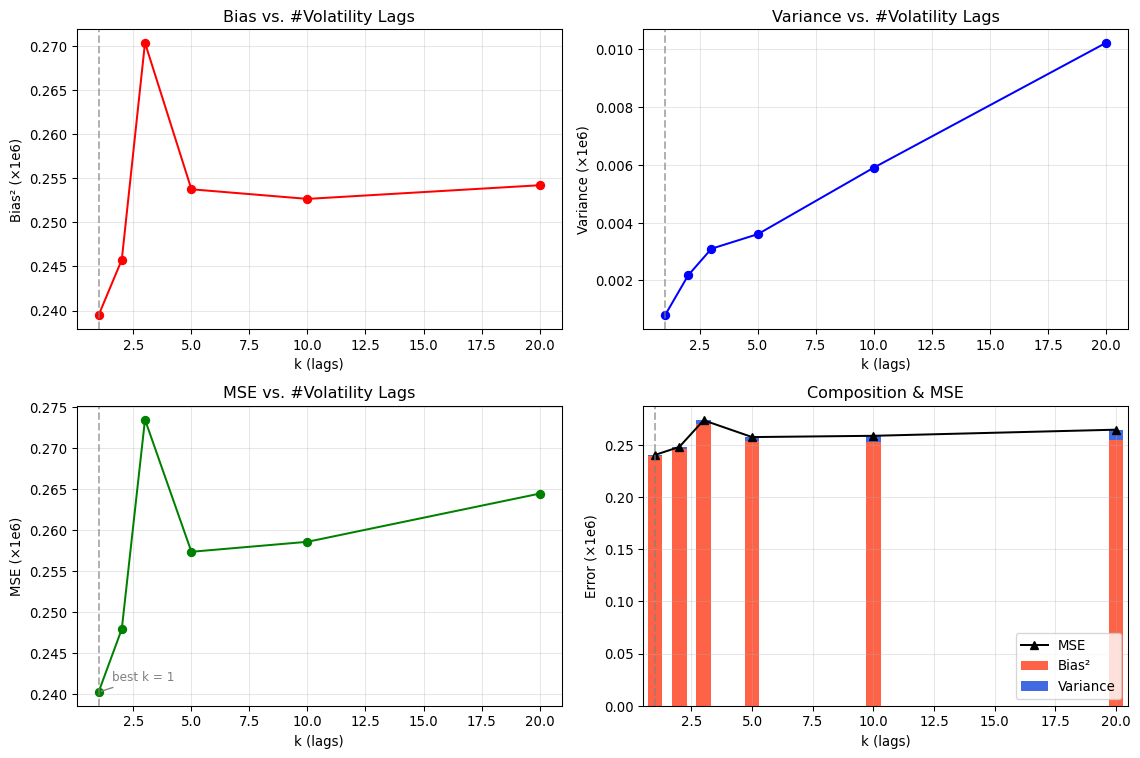

A more precise way to motivate model complexity is to recall the stylised facts of liquid asset returns. These empirical regularities shape both the features we build and the algorithms we choose, and they explain why the bias–variance trade‑off in finance often differs from textbook settings.

- Heavy tails and mild skewness

- Large moves occur more often than Gaussian models predict. Outliers and tail‑risk dominate error metrics.

- Implication: prefer robust losses, heavy‑tailed likelihoods, and careful validation; avoid “over‑confident” Gaussian assumptions.

- Weak autocorrelation in raw returns

- Daily (and lower‑frequency) returns have little linear predictability, though microstructure or frictions can induce small effects.

- Implication: complexity aimed at predicting mean returns risks overfitting; use strong regularisation and out‑of‑sample checks.

- Volatility clustering and long memory

- High‑volatility periods cluster, and |r| or r² show persistent autocorrelation.

- Implication: features using lagged volatility, realised measures, or GARCH‑style dynamics are helpful. In our bias–variance demo, model complexity is the number of volatility lags k : precisely to exploit this persistence.

- Asymmetry (leverage effect)

- Negative returns are followed by higher future volatility more than positive returns of the same magnitude.

- Implication: include sign‑sensitive terms or nonlinearities (e.g., EGARCH‑type features or interactions) when modelling risk.

- Time‑varying correlations and factor structure

- Assets co‑move through common factors whose loadings and correlations shift over time.

- Implication: dimension‑reduction and regularised multivariate models (e.g., shrinkage, dynamic factors) help control variance.

- Non‑stationarity and regime change

- Properties of returns evolve with policy, liquidity, and technology; parameters drift and break.

- Implication: use rolling/expanding windows, time‑aware cross‑validation, and adaptive models.

- Market microstructure effects at high frequency

- Bid–ask bounce, discreteness, and asynchronicity bias naive estimators.

- Implication: aggregate appropriately, de‑noise, or use models designed for irregular sampling.

These facts justify richer, carefully regularised models. Complexity can reduce bias by capturing nonlinearities and persistence (especially in volatility), but the variance cost must be controlled with robust features, penalisation, and time‑aware validation : themes made concrete in the volatility‑lag bias–variance demonstration that follows.

::: {.callout-important}

#### Theory Lens: Why These Facts Arise

Understanding the mechanisms behind the stylised facts helps you choose features and models with intent:

- Information arrival and variance mixing

- News and order flow arrive irregularly. If variance changes over time, returns look like a mixture of normals → heavy tails and volatility–volume comovement. Stochastic‑volatility and GARCH families formalise this.

- Heteroskedastic dynamics and gradual information diffusion

- Traders update at different speeds; large orders are split; herding/meta‑orders propagate. These behaviours generate volatility clustering and long memory in |r| and r². ARCH/GARCH, FIGARCH, and long‑memory filters capture the persistence.

- Efficient‑market baseline with microstructure frictions

- With fast competition, linear predictability in daily returns is weak. At very high frequency, microstructure (bid–ask bounce, discreteness, asynchronous trading) induces short‑horizon negative autocorrelation and biases naive variance estimates.

- Leverage and volatility‑feedback asymmetries

- Price drops increase financial leverage and can raise required returns; both channels raise future volatility more after losses than gains → the leverage effect. Nonlinear or sign‑sensitive features are appropriate.

- Time‑varying factor exposures and flight‑to‑quality

- Common drivers shift across states; correlations rise in stress. Dynamic factors and DCC‑style models allow covariances to evolve; shrinkage controls estimation error in high dimensions.

- Structural change and adaptation

- Policy, technology, and market design change DGPs. Structural breaks and regime switching imply parameters drift; use rolling/expanding windows, online updates, and explicit break/ regime models when needed.

These behavioural and microstructure channels link directly to modelling choices: lagged‑volatility features, heavy‑tailed likelihoods, dynamic covariance models, and time‑aware validation.

:::

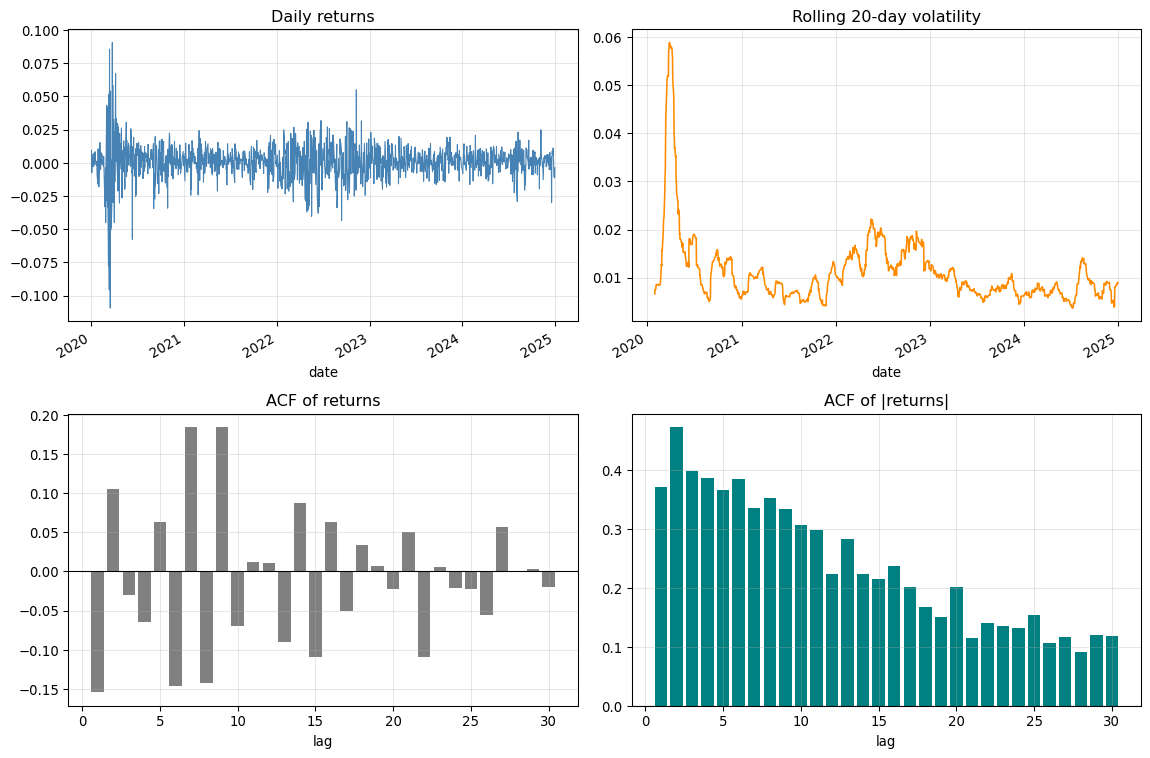

#### Volatility Clustering: Quick Demo

Volatility tends to arrive in clusters: tranquil periods alternate with turbulent ones. A quick way to see this is to compare the autocorrelation of raw returns (typically near zero) with the autocorrelation of absolute/squared returns (persistently positive).

::: {.callout-note}

Teaching notes : From fact to features

- Inspect the ACF of |returns| to guide the number of volatility lags k used as “complexity” in the bias–variance demo below.

- Prefer time‑aware train/test splits; re‑tune k if the ACF structure changes across regimes.

:::

```{python}

# Volatility clustering demo with Bloomberg database

import numpy as np, pandas as pd, matplotlib.pyplot as plt

def _fetch_close(symbol='SPY', years=5):

"""Fetch close prices from Bloomberg database."""

bbg = load_bloomberg(tickers=[symbol])

ticker_data = bbg.copy()

ticker_data['date'] = pd.to_datetime(ticker_data['date'])

ticker_data = ticker_data.set_index('date').sort_index()

# Filter to recent years

cutoff = ticker_data.index.max() - pd.DateOffset(years=years)

ticker_data = ticker_data[ticker_data.index >= cutoff]

return pd.DataFrame({'Close': ticker_data['PX_LAST']})

def _acf_abs(x, max_lag=30):

"""Simple ACF for absolute values."""

x = np.asarray(x)

x = np.abs(x) - np.abs(x).mean()

n = len(x)

var = (x**2).sum()

return np.array([(x[:n-l] @ x[l:]) / var for l in range(1, max_lag+1)])

df = _fetch_close('SPY', 5)

print(f"Loaded {len(df)} days of SPY data from Bloomberg database")

ret = df['Close'].pct_change().dropna()

fig, axs = plt.subplots(2, 2, figsize=(12, 8))

ret.plot(ax=axs[0,0], color='steelblue', lw=0.8)

axs[0,0].set_title('Daily returns'); axs[0,0].grid(alpha=0.3)

ret.rolling(20).std().plot(ax=axs[0,1], color='darkorange', lw=1.2)

axs[0,1].set_title('Rolling 20-day volatility'); axs[0,1].grid(alpha=0.3)

lags = 30

acf_r = [ret.autocorr(lag=i) for i in range(1, lags+1)]

axs[1,0].bar(range(1, lags+1), acf_r, color='gray'); axs[1,0].axhline(0, color='k', lw=0.8)

axs[1,0].set_title('ACF of returns'); axs[1,0].set_xlabel('lag'); axs[1,0].grid(alpha=0.3)

acf_abs = _acf_abs(ret.values, max_lag=lags)

axs[1,1].bar(range(1, lags+1), acf_abs, color='teal'); axs[1,1].axhline(0, color='k', lw=0.8)

axs[1,1].set_title('ACF of |returns|'); axs[1,1].set_xlabel('lag'); axs[1,1].grid(alpha=0.3)

fig.tight_layout(); plt.show()

print(f"Return ACF @lag1 ≈ {acf_r[0]:.3f}; |return| ACF @lag1 ≈ {acf_abs[0]:.3f}")

```

::: {.callout-tip}

Try it: Change the ticker (e.g., `AAPL`), the volatility window (10/60 days), or the number of lags. Observe that while returns have little autocorrelation, the absolute/squared returns show persistent autocorrelation : the hallmark of volatility clustering. This is why the bias–variance demo uses lagged volatility features.

:::

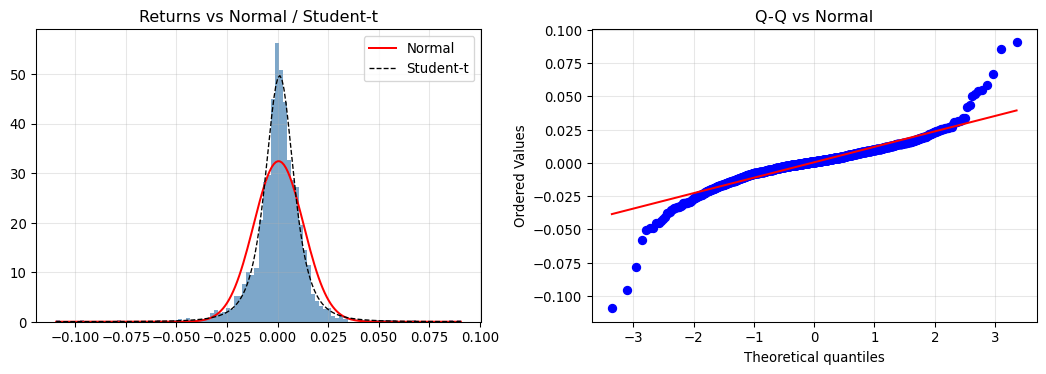

#### Heavy Tails: Quick Check

Financial returns exhibit fatter tails than the Normal model. This matters for risk estimates and confidence intervals.

```{python}

import numpy as np, pandas as pd, matplotlib.pyplot as plt

from scipy import stats

# Load SPY returns from Bloomberg database

bbg = load_bloomberg(tickers=["SPY"])

spy = bbg.copy()

ret = spy['return'].dropna()

print(f"Bloomberg SPY data: {len(ret)} daily returns")

skew = stats.skew(ret); kurt = stats.kurtosis(ret, fisher=True)

jb_stat, jb_p = stats.jarque_bera(ret)

fig, axs = plt.subplots(1, 2, figsize=(11, 4))

axs[0].hist(ret, bins=100, density=True, alpha=0.7, color='steelblue')

x = np.linspace(ret.min(), ret.max(), 200)

axs[0].plot(x, stats.norm.pdf(x, ret.mean(), ret.std()), 'r-', lw=1.5, label='Normal')

params = stats.t.fit(ret)

axs[0].plot(x, stats.t.pdf(x, *params), 'k--', lw=1.0, label='Student-t')

axs[0].set_title('Returns vs Normal / Student-t'); axs[0].legend(); axs[0].grid(alpha=0.3)

stats.probplot(ret, dist='norm', plot=axs[1]); axs[1].set_title('Q-Q vs Normal'); axs[1].grid(alpha=0.3)

plt.tight_layout(); plt.show()

print(f"Skew={skew:.3f}, Excess kurtosis={kurt:.2f}, JB p-value={jb_p:.2e}")

```

::: {.callout-note}

Teaching notes: Heavy tails inflate risk relative to Gaussian assumptions. Prefer robust losses, heavy‑tailed likelihoods, or quantile‑based risk metrics when appropriate.

:::

#### Stationarity: ADF Check

Many models assume (weak) stationarity. Prices are usually non‑stationary; returns often stationary. Always check.

```{python}

import numpy as np, pandas as pd

try:

from statsmodels.tsa.stattools import adfuller

except Exception:

adfuller = None

# Load SPY from Bloomberg database

bbg = load_bloomberg(tickers=["SPY"])

spy = bbg.copy()

spy['date'] = pd.to_datetime(spy['date'])

spy = spy.set_index('date').sort_index()

prices = spy['PX_LAST'].dropna()

ret = spy['return'].dropna()

print(f"Bloomberg SPY: {len(prices)} prices, {len(ret)} returns")

if adfuller is not None:

adf_price = adfuller(prices, autolag='AIC')[1]

adf_ret = adfuller(ret, autolag='AIC')[1]

print(f"ADF p-value (price): {adf_price:.3e} : likely non-stationary")

print(f"ADF p-value (returns): {adf_ret:.3e} : often stationary")

else:

print("statsmodels not available; skipping ADF test")

```

::: {.callout-note}

Teaching notes: Use transforms (log‑diff/returns), rolling windows, and time‑aware CV when stationarity is questionable or regimes change.

:::

### The Three Prediction Problems in Finance {#sec-three-prediction-problems}

The stylised facts we have reviewed reveal a fundamental asymmetry that shapes everything in financial data science: **what you can predict depends on what you're trying to predict**. Traditional textbooks often present time series models (ARIMA, GARCH) as a technical progression, implying that more sophisticated models yield better predictions. But this framing obscures a more important question: *where is the signal?*

Financial prediction divides into three distinct problems, each with different signal strength and appropriate methods:

| Problem | Target | Typical R² | Best Approach | Economic Value |

|---------|--------|------------|---------------|----------------|

| **The Mean** | Future returns | 1-2% | Naive forecast often wins | Low (after costs) |

| **The Variance** | Future volatility | 15-40% | GARCH family | High (options, VaR, allocation) |