Understanding Market Manipulation: Theory and Practice

A Teach-In Event for the FCA Tech Sprint on Market Abuse Surveillance

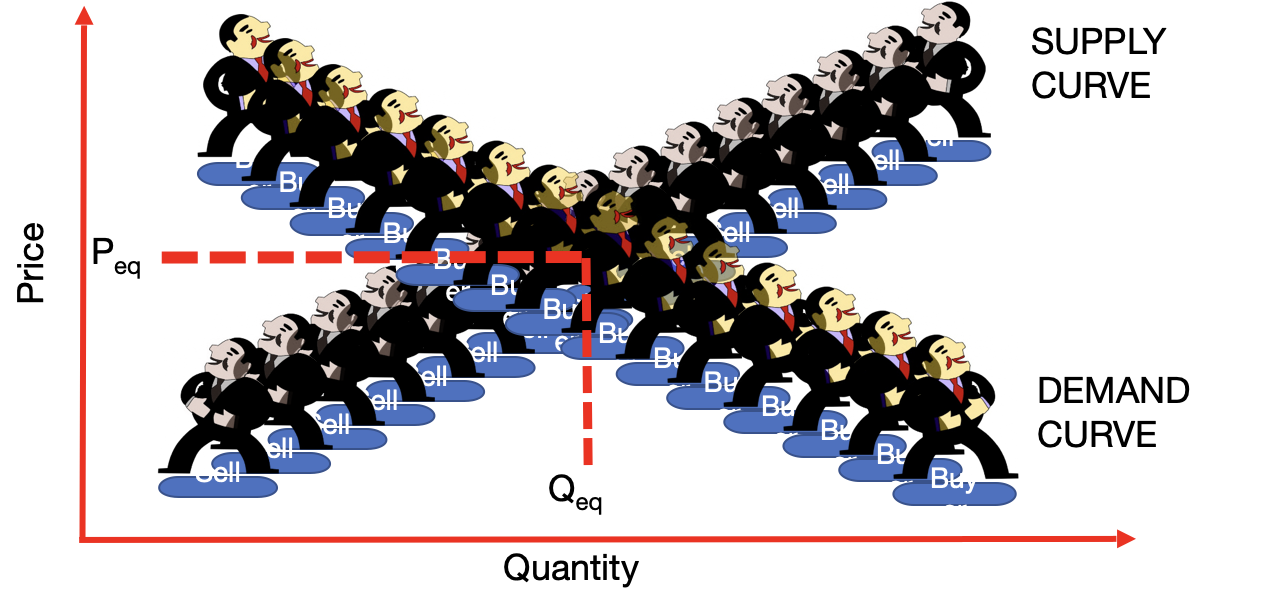

How Trader Activity Informs Market Prices:

Econ 101 View

- Supply and Demand Dynamics

- Supply: Sellers willing to sell at various price points

- Demand: Buyers willing to buy at various price points

- Equilibrium price: Where supply meets demand

- Atomised View of Trader Activity

How Trader Activity Informs Market Prices

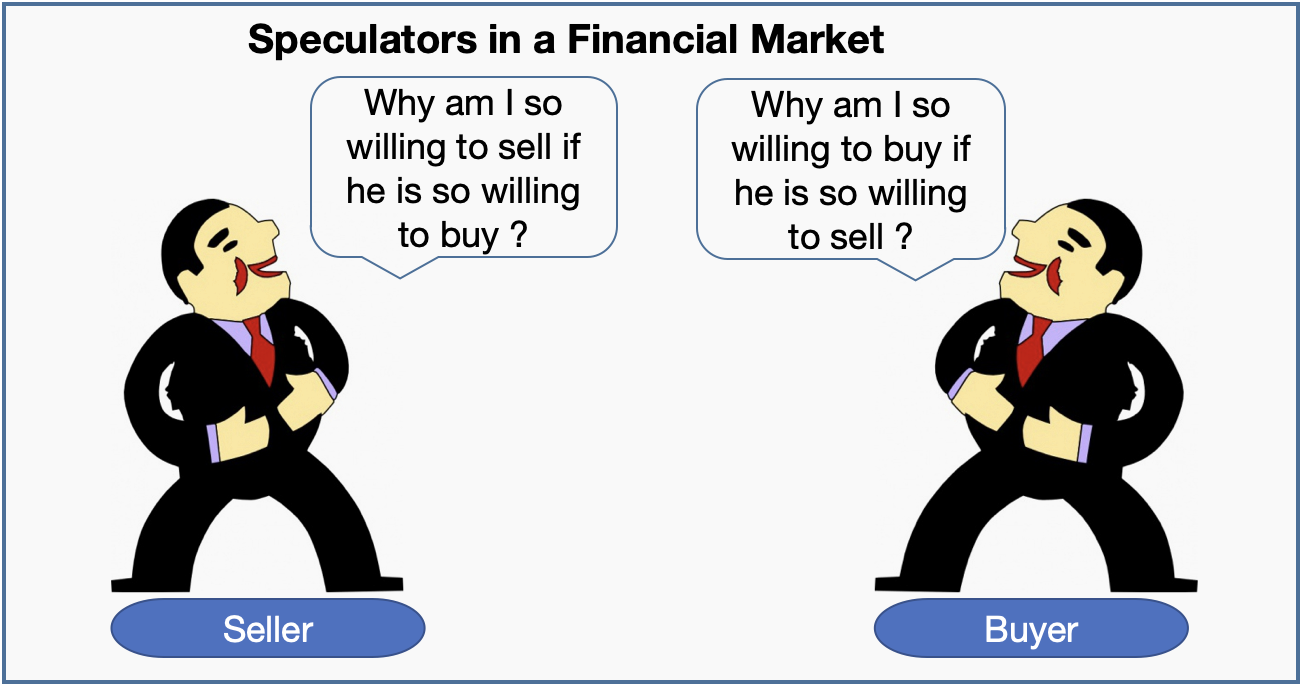

The Trading Paradox

- High trading volume seems paradoxical

- Rational traders should be skeptical of willing counterparties

- “Why is the other party willing to trade with me?”

- Yet, we observe high turnover in financial markets

- This paradox challenges our understanding of price formation

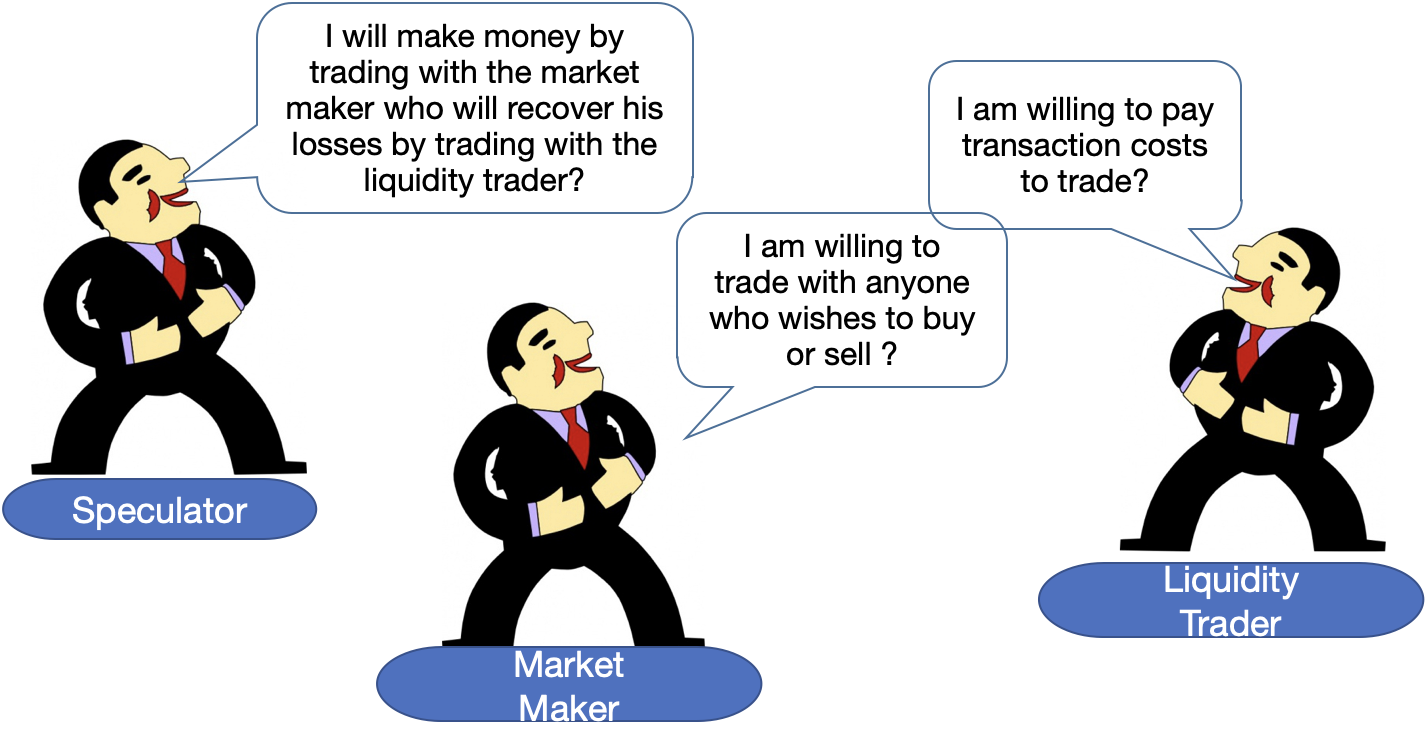

Resolution: Three Key Market Participants

- Liquidity Traders

- Trade for non-information reasons (e.g., cash needs, rebalancing)

- Willing to pay transaction costs to meet trading needs

- Market Makers

- Provide liquidity by always being willing to buy or sell

- Profit from the bid-ask spread

- Lose to informed traders, but recover losses from liquidity traders

- Speculators (Informed Traders)

- Trade based on information or analysis

- Profit from trading against less informed participants

References

![]()

Aggarwal, Rajesh K, and Guojun Wu. 2006. “Stock Market Manipulations.” The Journal of Business 79 (4): 1915–53.

Allen, Franklin, and Douglas Gale. 1992. “Stock Price Manipulation.” The Review of Financial Studies 5 (3): 503–29.

Barberis, Nicholas, and Richard Thaler. 2003. “A Survey of Behavioral Finance.” In Handbook of the Economics of Finance, 1:1053–1128. Elsevier.

Benabou, Roland, and Guy Laroque. 1992. “Using Privileged Information to Manipulate Markets: Insiders, Gurus, and Credibility.” The Quarterly Journal of Economics 107 (3): 921–58.

Glosten, Lawrence R, and Paul R Milgrom. 1985. “Bid, Ask and Transaction Prices in a Specialist Market with Heterogeneously Informed Traders.” Journal of Financial Economics 14 (1): 71–100.

Kyle, Albert S. 1985. “Continuous Auctions and Insider Trading.” Econometrica 53 (6): 1315–35.

Mei, Jianping, Guojun Wu, and Chunsheng Zhou. 2004. “Behavior Based Manipulation: Theory and Prosecution Evidence.” Available at SSRN 457880.

Meulbroek, Lisa K. 1992. “An Empirical Analysis of Illegal Insider Trading.” The Journal of Finance 47 (5): 1661–99.

Shleifer, Andrei. 2000. Inefficient Markets: An Introduction to Behavioral Finance. Oxford University Press.

Van Bommel, Jos. 2003. “Informed Trading, Market Manipulation and Price Volatility.” Journal of Financial Intermediation 12 (3): 201–27.